Vladimir Lenin, who knew a thing or two about revolutions, apocryphally said, “There are decades where nothing happens; and there are weeks where decades happen.” This year was most certainly the latter: from trade wars to real wars and markets reaching dizzying new heights, all with the backdrop of a revolution in computing.

You could be forgiven for thinking we have been through a market cycle, rather than a period of unbroken economic growth and upward stock markets. If you had told me in April, as markets were in freefall from US President Donald Trump’s Liberation Day tariffs, that global markets would be up 14% year to date (in sterling) I would have offered to eat my shoe. And yet, here we are, amid new market highs, dominated by the still nascent AI theme.

The drive for AI is insatiable, following two dominant years in 2023 and 2024, the concentration in markets has become eyewatering. The chart below shows how different types of US companies have ebbed and flowed over time. ‘Defensives’, which tend to be less sensitive to changes in economic growth, and ‘cyclicals’, which are more geared to the ups and downs of the economy, have traded predominance over past decades. Yet today, you can see both have shrunk before a tech-trained one-trick pony.

FOMO builds among investors

The investing world is hunting for opportunity in the rush for AI exposure, with a marked increase in the number of leveraged ETFs hitting the market this year. More worrisome is the number which are single-stock, allowing for leveraged bets. We started 2025 with a total of 42 leveraged single-stock ETFs; this more than doubled in the first four months of the year. There’s a lot of highly speculative bets being made by tourist investors with FOMO (‘fear of missing out’). That sort of behaviour can cause volatility to spike when the mood turns. Maybe the mood music has been changing a bit over the last few weeks? Yet that doesn’t mean markets must plunge and remain depressed. These chaotic unwindings often provide opportunities to buy the good that’s been chucked in with the bad.

We aren’t in the business of calling the tops or bottoms of markets – that’s often a fool’s game. But we do recognise the importance of diversification in protecting our clients’ money. Below shows our sector exposure as at the end of September: we’re far from a one-trick tech pony.

Everyone wants to be an AI king, not everyone will wear a crown

The AI theme has been a major driver of returns for investors over the last three years. We’re not naysayers to the new digital age, quite the opposite with around 20% of our fund aligned to the theme. Our issue lies in the market’s belief that every company talking about AI will be an AI winner. The below table suggests over 40% of the US market consists of AI stocks, we are not so sure. We think a more concentrated number of players will dominate the adoption of AI.

Are AI stocks really 43% of the S&P 500?

When you look back through history, feverish buying, driven by a fear of missing out, usually leads to corrections. Without a crystal ball showing the future growth engine of markets, we provide investors with a well-diversified portfolio of high-quality businesses that should be able to perform over the market cycle. Investing is a long game.

Having managed this fund for over 22 years, I’m very aware of the impact a sudden change in markets can have on a fund’s performance. Whether that be a degradation in the fabric of our financial system like in 2008; a China-driven market rout in 2015; a global pandemic in 2020, or the inflation shock of 2022. These experiences have taught me to be adaptable in portfolio construction, and humble about what you can’t know.

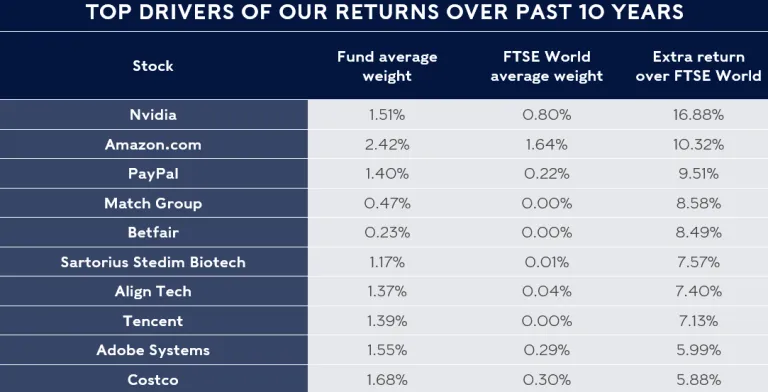

Our approach is never to put all our eggs in one rocket-fuelled investment basket. We keep prudent position size limits in place (typically 4% is the ceiling for a single stock) to reduce the risk of any one company tripping up. But our true differentiator is investing in underappreciated and under-owned high-quality growth businesses. Our fund’s ‘active share’ is 81%, meaning the portfolio composition is overwhelmingly different to the FTSE World global equity index.

This active share can be difficult to envisage, so here’s a table of the 10 stocks that have delivered the most returns for our fund over the 10 years to 31 December 2024, the latest we have figures for. You can see that we have gained much of our fund returns from stocks that really weren’t a big part of the world index at all. (Note, some of these companies we no longer hold.)

Source: StatPro, Rathbones; 10 years ended 31 Dec 2024.

Past performance should not be seen as an indicator of future performance.

Boring stocks usually make the best weather-proofing

We’re not calling the end of AI, far from it. But for those investors who are nervous about valuations and the hyper(scaler)-concentrated nature of markets may be reassured to know that we maintain a defensive basket of recession-resistant stocks. From waste collection to healthcare, this portion of the fund, around 20%, consists of companies with products and services that tend to be the last to be cut from people’s spending budget. During a risk-off scenario, they add ballast to our portfolio, often trading up or flat versus a down market. And what better test case than Liberation Day (2 April)?

Bifurcation in views on the future of global equity markets continues to widen. With no one able to see the future, we believe now more than ever that it’s essential to have diversification in your portfolio, invested in high-quality businesses able to move with innovation, not fight it.