Article last updated 30 September 2025.

Will the extraordinary quantity of monetary and fiscal stimulus result in abnormally high inflation? Words to that effect form one of our most frequently asked questions this year. It’s an important one: returns from ‘fixed income’ assets such as conventional bonds can be decimated by unanticipated inflation, and although equities tend to do best in periods of slightly above-average inflation, very high inflation is a threat to their returns too.

High inflation is one of our three key risks to the economic recovery from COVID-19, alongside persistently high unemployment and a second wave of fatalities. But it is the one to which we assign the lowest probability. This conclusion is predicated on two broad observations.

Disease is different to war

“Pandemics affect demand for goods and services more than they do their supply. In this respect, disease is very different to war.”

First, the history of global pandemics since the 14th century or regional epidemics in the 20th century suggests that they affect demand for goods and services more than they do their supply. In this respect, disease is very different to war. With all other things being equal, less demand for something relative to its supply causes prices to fall. Today, price data, business surveys and observations from analysts in China, which is a little further down the road to recovery than the rest of the world, suggest we’re following a similar pattern. And though it is early on, business surveys in Western countries, such as the Purchasing Managers’ Indices, also show how activity rebounded in June while prices remained depressed.

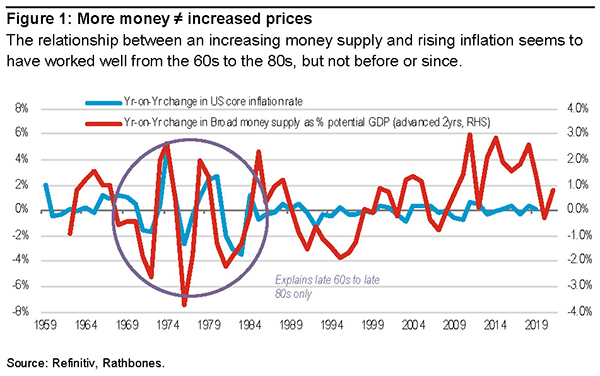

More money ≠ increased prices

Our second broad observation is that a rapid increase in money doesn’t necessarily lead to rapid inflation. ‘Printing money’ to stimulate the economy, as it’s often referred to euphemistically, is nothing new. Many commentators warned of sky-high inflation after central banks first expanded their balance sheets with then-novel “quantitative easing” programmes (QE) in 2008. But the lesson from the subsequent decade is that an increase in central bank money on its own is not sufficient to induce inflation. Consumer prices were stuck far below central banks’ inflation targets for most of that period.

Commentators touting inflation often cite Milton Friedman, one of the few economists familiar to non-economists. But his ‘monetarism’ in its most simplistic form (ie. central banks print money, inflation goes up) does not hold empirically. It worked well from the late 1960s to the late 1980s, but not so much before and certainly not since. We do not believe the relationship is likely to reassert itself.

“The lesson from the last decade is that an increase in central bank money on its own is not sufficient to induce inflation.”

That’s actually not even how it’s taught in undergraduate textbooks anymore. The best bits of Friedman have been added into frameworks that do a much better job of explaining how economies work because they distinguish two factors in particular: (i) the type of money that’s being created and the role of commercial banks; (ii) the so-called ‘velocity of money’ – the rate at which money is spent and re-spent.

Although the latter is a rather abstract concept, it is an extremely important one. ‘Monetarists’ believe that the velocity of money can be ignored because it is either constant, or just responds to other things, such as the supply of money. But that doesn’t appear to be correct. Indeed, ever a social scientist to be admired, Friedman himself admitted towards the end of his long life that the velocity of money is actually an independent variable, and the new research backing that up is credible. You could think of it like this: inflation depends not just on the money supply but on the public’s willingness to use it. The problem today (and, indeed for the last 30 years) is that people want to hoard money, and that’s disinflationary. It’s also why interest rates have trended down. Is that behaviour likely to change in the foreseeable future?

Back to the first point, the type of money matters because central banks actually create a tiny fraction of what most of us think of as money. The economist Richard Werner estimates that in normal times, commercial banks create 97% of total UK money creation, mainly by depositing a loan into someone’s bank account. Recent surveys of lenders point to a tightening of available credit supply to households in the US, the UK and the eurozone - understandably given the prospect of high unemployment. Lending conditions for firms would have tightened further but for government loan guarantees and other measures, which were a one-time deal to plug the hole in corporate cash flow made by stay at home orders. Governments can print money, but if commercial banks aren’t lending it out at the same multiple, inflation is likely to be contained.

Remaining below capacity

As we return to some semblance of normality, it’s likely commercial banks will remain relatively cautious about creating new loans, and firms and households will remain relatively cautious in their spending and investment behaviours. That would depress that velocity of money, exerting a disinflationary impulse.

For sure, our research suggests that it is unlikely that this recession will be accompanied by a banking crisis. That means that inflation is likely to be held back less forcefully than it was after 2008 because we won’t be grappling with the prolonged deflationary aftermath of such crises, which entail huge deleveraging. But corporate saving will likely be a little higher due to the need for many companies to pay back some of the emergency loans that have been dished out so far. Household saving may also remain elevated as people continue to worry about their jobs. Employer surveys have suggested as many as a quarter of furloughed staff in the UK may end up redundant. Combine increased saving/decreased spending with the likely increase in business failures over the next 12 months and we have a situation in which the economy, while improving, is likely to operate below capacity for quite some time. Even in our most optimistic simulation, the UK economy doesn’t converge on the level of activity estimated by the pre-crisis trend until 2022 – and our base case is much later than that. When the economy is operating below trend, any increase in the money supply should initially drive output back to trend without generating high inflation.

National debt and credibility

So far, we have discussed that the demand for money matters for inflation as much as its supply. Institutions also matter. A government’s credible commitment to price stability anchors inflation expectations and explains many periods of benign prices. Today, some investors worry that the ‘monetisation’ of government debt – government spending funded by debt that is then bought by central banks with newly created money – marks a reneging of that credible commitment, the beginning of what some commentators call ‘fiscal dominance’.

We disagree. For sure, central banks and government treasuries are working together more closely. But that doesn’t mean central bankers are throwing away their inflation targets or their mandates to ensure financial stability, and instead doing whatever the government tells them to do. For years, some central bankers, such as Mario Draghi, the former head of the ECB, have shouted that without fiscal stimulus, developed economies may be mired in deflation. It’s not a paradigm shift for the inflation regime when inflation-targeting central bankers are getting what they’ve asked for!

Turning to the evidence, a number of cross-country and single-country studies have found no statistically significant correlation between fiscal deficits and inflation, regardless of whether deficits are funded with debt sold to the private sector or central bank monetisation. Although people focus on well-known examples of hyperinflation, such as Weimar Germany or late-1980s Latin America, there are many examples where debt monetisation hasn’t resulted in inflation. For example, Japan and the US in the 1930s, or Canada and New Zealand after WW2. That’s because markets have understood the objective: a short period of money-financed government spending in order to plug a hole in the economy from which profound deflationary forces would otherwise spring.

Where money-financed spending has resulted in hyperinflation, deficient institutions and a lack of political capital is invariably to blame. Those invoking the Weimar example should note that hyperinflation ended in Germany and its central European neighbours in the 1920s a few months before the money supply stopped rising at an eye-watering rate. It ended with institutional reform.

Demystifying de-globalisation

Does the possibility of de-globalisation change things? First, it’s important to realise that trade as a share of global GDP peaked in 2007. The globalisation impulse – which is what would drive down prices year after year – is arguably long behind us. Second, even before this, globalisation hasn’t been as deflationary as the popular view likes to suggest. Of course, it’s pressed down greatly on the cost of producing tradeable goods, but at the same time it has unleashed more demand for tradeable goods - especially fuel, food and raw materials - by enriching countries like China. Some academic studies which have attempted to draw all of these offsetting forces together suggest that globalisation, even when in full swing before 2007, was only mildly deflationary.

Of course, de-globalisation is a risk, but we are not seeing evidence of the trend just yet. The US trade deficit is wider than ever, China’s share of global trade has jumped higher this year. De-globalisation could be mandated by governments, but left to the free market it’s unlikely because the rational solution to supply-chain vulnerability exposed by COVID-19 is supply-chain diversification not repatriation – you don’t want to source all of your widgets from China anymore but you don’t want to source them from any other single country anymore either, including your own. Indeed, a recent study found that the US manufacturers that weathered the first month of COVID-19 the best were the ones with the most diversified supply chains.

Finally, if increasingly populist and nationalistic governments become more protectionist that would push up prices. But this forced change in input costs would lead manufacturers to adopt roboticised and automated processes at a much faster rate, which would push prices back down.

Long-term trends look benign

It’s also worth considering the inflation implications of any structural shifts which might be catalysed by the COVID-19 crisis. Most of the ones we can think of (eg. a greater shift from the physical to the digital economy, or a move away from city-centre commercial real estate) are also mildly disinflationary.

“Those suggesting the 1970s is a roadmap for today are ignoring some important points of economic topography.”

Three years ago, we conducted a review into the long-term drivers of inflation. Although there are competing theories, we concluded that ageing populations are likely to be inflationary. In short, retirees continue to buy goods and services at a reasonable pace, but with relatively fewer people of working age to produce them prices are pushed up. Japan is the exception that proves the rule. This process was at work there too, but, unusually, its workers had invested their savings abroad and as they repatriated them to fund their retirement the Yen appreciated and so Japan ‘imported’ deflation. Nevertheless, this process is only likely to exert a very small amount of upward pressure on inflation over the next decade in the UK or US, who are ageing relatively slowly.

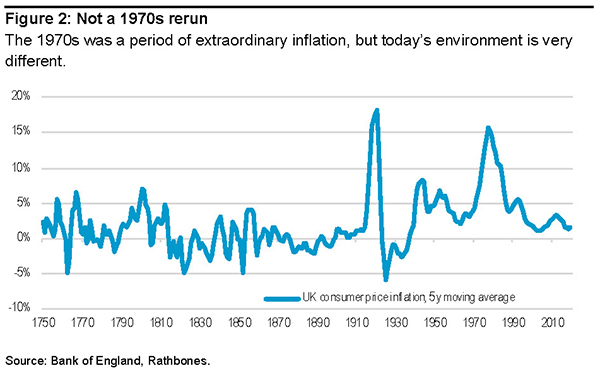

Not a 1970s rerun

The 1970s was a period of extraordinary inflation. If you look at a chart of UK inflation going back a few hundred years, the 1970s was the anomaly, not today. The 1970s is really quite unlike the present. Key differences today include: increasingly restrictive banking regulation; spare capacity in the economy and excess unemployment; no exchange rate regime to be broken; structurally constrained oil prices; the credibility of central bank’s inflation targets; a lack of inflation-linked wage contracts, preventing a wage-inflation spiral; financial innovation and technological disruption. Those suggesting the 1970s is a roadmap for today are ignoring some important points of economic topography.

Low inflation is the bigger risk

"We are more concerned about the risk that inflation remains stubbornly low than we are about it becoming intolerably high.”

We are more concerned about the risk that inflation remains stubbornly low, even if the recession is short-lived, than we are about it becoming intolerably high. To sum up, inflation is about more than central bank money. It is about how commercial banks turn money into a supply of credit, and about the private sector’s demand for money. With spare capacity in the economy and incentives for companies and households to hoard cash, inflation should remain tamed. The institutional environment also matters, and the nature of central banks’ and treasury departments’ relationship remains credible. This has allowed nations to engage in debt monetisation before, without huge inflation.

All that said, we must emphasise once again that the unprecedented nature of this shock means that there is considerable uncertainty as to how the economics of it all plays out. We will certainly monitor early indicators of inflation in case our thesis is wrong. For now, we think the risks are contained.