Article last updated 30 September 2025.

COVID-19, and the disruption to life and economic activity it has wrought, are new to mankind. From its previous peak, America’s benchmark S&P 500 Index has experienced its fastest 20%+ fall since its inception in 1957. Drops of that magnitude – signalling a bear market – have on average taken over 200 days. But the record-breaking plunge is not a reason to expect a sharp technical rebound to begin soon. It simply reflects the gravity of the situation and the fact that markets have been blindsided.

When it first became apparent that COVID-19 was rapidly spreading around the globe, we wrote about three possible scenarios; a rapid dissipation of the virus and rebound in economic activity being the most optimistic. Now the likelihood that normalisation occurs in the second quarter (Q2) is as good as zero. Indeed, it is now widely expected that developed market GDP will suffer the largest quarter-on-quarter contraction in modern history in the three months to the end of June. Morgan Stanley, for example, forecasts a contraction of 7.25%, or a whopping 30% drop in annualised terms. Others, such as Capital Economics and Oxford Economics, forecast even larger quarterly slumps of 10% and 11%, respectively.

Broadly speaking, the two scenarios we are left with are: (i) an almighty contraction in Q2, spilling over into Q3, but giving way to a very strong rebound in the final three months of the year; or (ii) an almighty contraction in Q2 with subdued activity and profits lasting into 2021. We don’t believe anyone can say which of the two is more likely with any rigour. It’s not just about the epidemiology, but also governments’ social responses and their electorates’ tolerance of them.

Nevertheless, we have calculated that 2,200 would be roughly fair value for the S&P 500 in scenario (ii) – at its 23 March low the index was at 2193. We believe the market is pricing in a very high chance of the worst-case scenario. Given we cannot say that scenario (ii) is more likely than scenario (i), the risks appear asymmetrical and we believe there is more scope for equity markets to rise from today’s level than fall.

That’s not to say that we believe stocks have reached their bottom and will start rising now, or even next month. Of course, markets can temporarily overshoot on the way down to ‘fair value’, and there is a significant possibility that equities will hit new lows. But we represent long-term investors, and we’re not in the business of trying to time the market with perfection in highly uncertain situations.

Throwing the kitchen sink at it

The monetary policy response to the virus’ disruptive force has been extraordinary in both scale and timeliness, greatly increasing the likelihood that activity will rebound strongly when social distancing measures are removed.

Central banks have flooded the financial system with liquidity and have specifically targeted stressed markets, including but not limited to such steps as commercial paper purchases, buying investment grade corporate bonds at issue, buying on the open market bonds, bond ETFs, and securities backed by small business and consumer loans, and offering cost-free funding for small and medium-sized businesses. Fiscal policy has also been extraordinarily targeted and timely. Though slower to emerge in the US, Congress has now agreed an extraordinary programme that will deliver direct stimulus equivalent to 5% of 2019 GDP, with more money available as business loans.

But some commentators have been voicing an optimistic belief that we would caution against – we think the notion that the stimulus will prevent markets from falling any further is unrealistic. In the midst of the global financial crisis in early 2008, then-President George W Bush authorised a $168 billion stimulus; in October 2008 US Congress approved the $700bn Troubled Asset Relief Program, which injected money into banks, mortgage markets and car companies; President Barack Obama’s $787bn American Recovery and Reinvestment Act was passed in February 2009. But markets didn’t finally trough until March 2009.

Central banks must keep providing as much dollar liquidity as the private sector needs. Initial programmes have been successful at staving off a crisis of dollar funding that was spreading around the globe as even the safest assets like gold and US Treasuries were being dumped in the ‘dash for cash’.

A stress test for dividends

As mass shutdowns cause a sudden and sharp drop in cash flow for many companies, the threat to dividend payments is a great concern for many investors, especially our clients who rely on them for income. Cuts to dividends may indeed be larger than normal; many issuers are in hard-hit sectors, have more debt on their balance sheets (‘financial gearing’), and pay very high dividends relative to their net income to start with.

Ordinarily maintaining dividends would be a priority for management teams, but we are in extraordinary circumstances. That may make managers feel less blameworthy for cutting unaffordable dividends, especially if other companies are cutting too. Even as long-term investors we should prepare for this eventuality. There are some areas of the market which will clearly see more significant downside to earnings, such as travel, leisure, retail, oil and mining. Where this is coupled with high levels of debt relative to earnings and cash flow, this will at a minimum lead to dividend cuts, if not financial distress and restructuring (potentially a bad outcome for equity holders) or even bankruptcy. Consumer staples and healthcare companies ought to maintain or increase their dividends even in tougher economic conditions given the relatively less cyclical nature of their demand. Travel, leisure and retail companies are in the eye of the storm and if they carry higher gearing they will likely need to cut dividends.

Even companies with hitherto conservative and appropriate levels of financial gearing could face distress in these exceptional economic circumstances. This is leading them to reassess dividends, which are usually considered a measure of a company’s strength, prestige and dependability, nowhere more so than in the UK. In this environment management teams will probably err on the side of caution and, if in doubt, suspend dividends now during the period of maximum uncertainty, potentially reinstating them later in the year once the crisis has been dealt with and economic activity returns to more normal levels.

The ultimate extent of dividend cuts depends on how quickly the coronavirus can be brought under control. If containment measures are less successful than they have been for example in China and South Korea, and have to be kept in place for longer than two to three months, then many if not most companies may have to suspend or at least reduce payments.

Rising defaults ≠ financial crisis

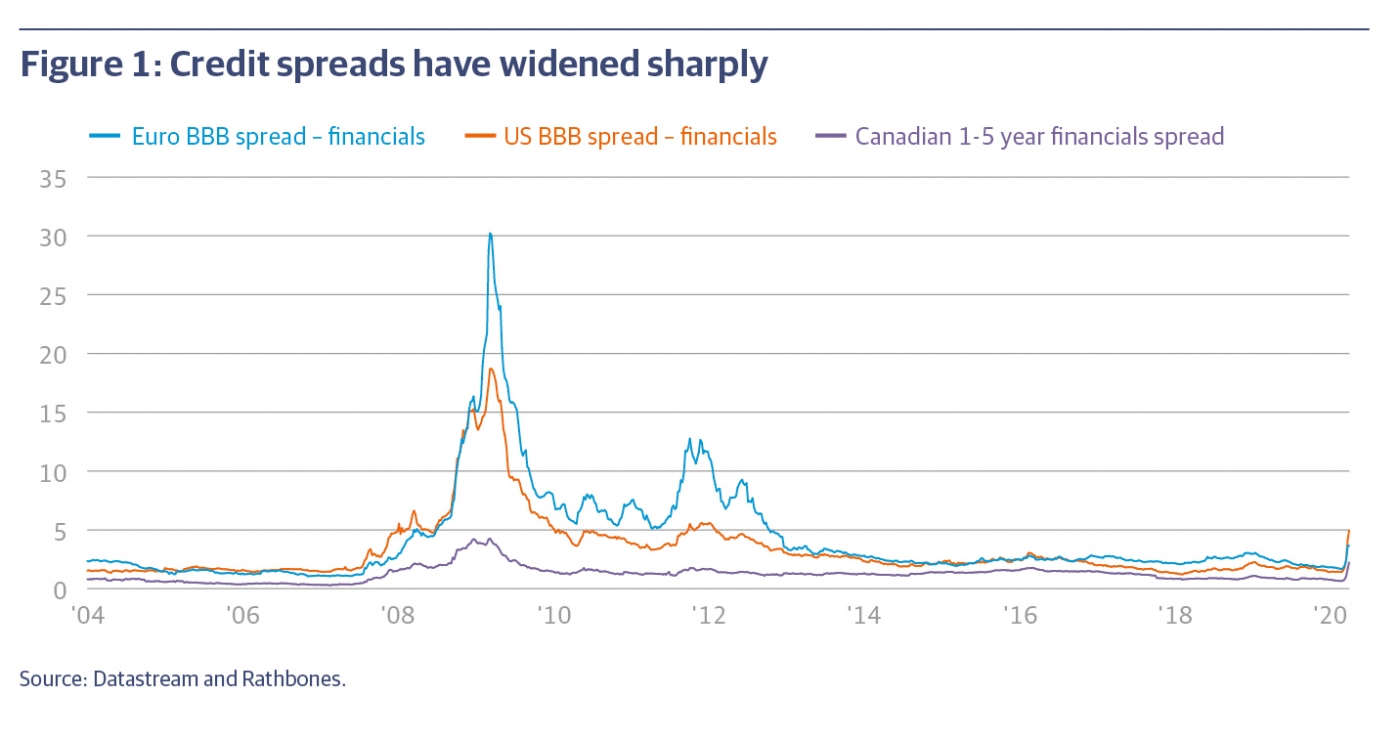

Before central banks stepped in with their extraordinary measures, liquidity was rapidly drying up in the corporate bond markets. Everyone was selling and no-one was buying. In the wake of the unprecedented central bank action, some liquidity had started to come back into corporate bond markets, but they remain under pressure.

Before the pandemic, we were already wary of the low level of compensation on offer for taking on the additional risk of investing in corporate bonds (or ‘credit’) relative to safer government debt. The main measure of this premium is called the spread, or the gap in yields between bonds of different credit qualities. These spreads have since risen dramatically, especially for the poorest quality, or high yield, debt. The spread between BB-rated and BBB-rated credit (straddling so-called ‘high yield’ and better-quality investment-grade debt) is back to 2009 levels, vindicating our caution. This underlines the huge risk, especially to passively traded corporate bond funds.

We may see many more corporate defaults, and certainly more ratings downgrades, than you would normally see in a short recession, but that doesn’t make it a financial crisis (see more on why we think this is unlikely in the “Financial risks remain” section of our previous InvestmentUpdate). Banks are unlikely to fail and a prolonged period of deleveraging and the deflation of real assets is unlikely.

Emerging market debt (EMD) has also seen spreads widen considerably, but we don’t think the higher compensation is worth the risk of adding exposure to these markets, many of which may bear the brunt of COVID-19 without having the resources to combat it. Turkey and South Africa in particular are at risk of default, and a default by either could cause contagion across all EMD markets.

The dash for cash

Yields on UK gilts, along with other major government bonds, initially plummeted as investors piled into safe-haven assets (yields move inversely to prices). But as panic spread through the markets, even assets normally considered ‘as safe as houses’ were being sold in the dash for cash. From their lows of around 0.25%, 10-year gilt yields surged back up, touching almost 1% in intraday trading in the height of the panic.

The move suggested investors may be wary of the coming surge in budget deficits to finance unprecedented levels of government stimulus. But we don’t believe UK or US bonds are at risk of a substantial sell-off in response to wider budget deficits. Bond investors aren’t even shunning Italian government debt, even though there remains the troubling nexus between the health of Italian banks and the government’s finances, which are much more indebted than the UK or US governments’.

The medium to longer term outlook for gilt yields needs to be monitored carefully as the situation develops. But for the near term at least we don’t think a large increase is yields is likely while the coronavirus crisis plays out and demand for safer assets continues. We therefore see gilts as preferable to cash.

Foundations of gold

Gold also suffered a significant setback after initially rallying on the COVID-19 outbreak. Gold, which tends to trade inversely to the dollar, took a fall amid the global dash for dollars. It’s most likely that investors were using their gold positions as a source of liquidity. We’ll be looking more into the performance of gold during and after liquidity-driven sell-offs at times of market stress, but for now we believe that gold is supported by solid underpinnings.

Gold’s brief sell-off may have also been driven by a rise in real rates (interest rates less inflation expectations) as inflation expectations fell in the early reaction to the coronavirus outbreak. Inflation expectations were already very low to begin with, and fears of a deflationary bust in the global economy pushed them lower still. However, they have since stabilised, and we don’t think real rates are likely to increase meaningfully in the near term. Indeed, the flood of central bank and government stimulus is also leading to some speculation that inflation could take off once recovery comes, though we also see this as unlikely given a number of structurally disinflationary trends (see our 2017 inflation report Under Pressure? for more on this subject).

If COVID-19 is to be a deflationary bust, the natural hedge is usually long-dated (long duration) bonds. But in the current unusual environment of negative real yields, the cost of carry (income foregone) for holding gold is far lower than it would be normally, making it more attractive even in this scenario. If the coronavirus turns out to be a temporary supply shock, and the barrage of demand-focused monetary and fiscal stimulus then fuels rising inflation expectations, potentially pushing real yields even lower, then gold should also respond well.

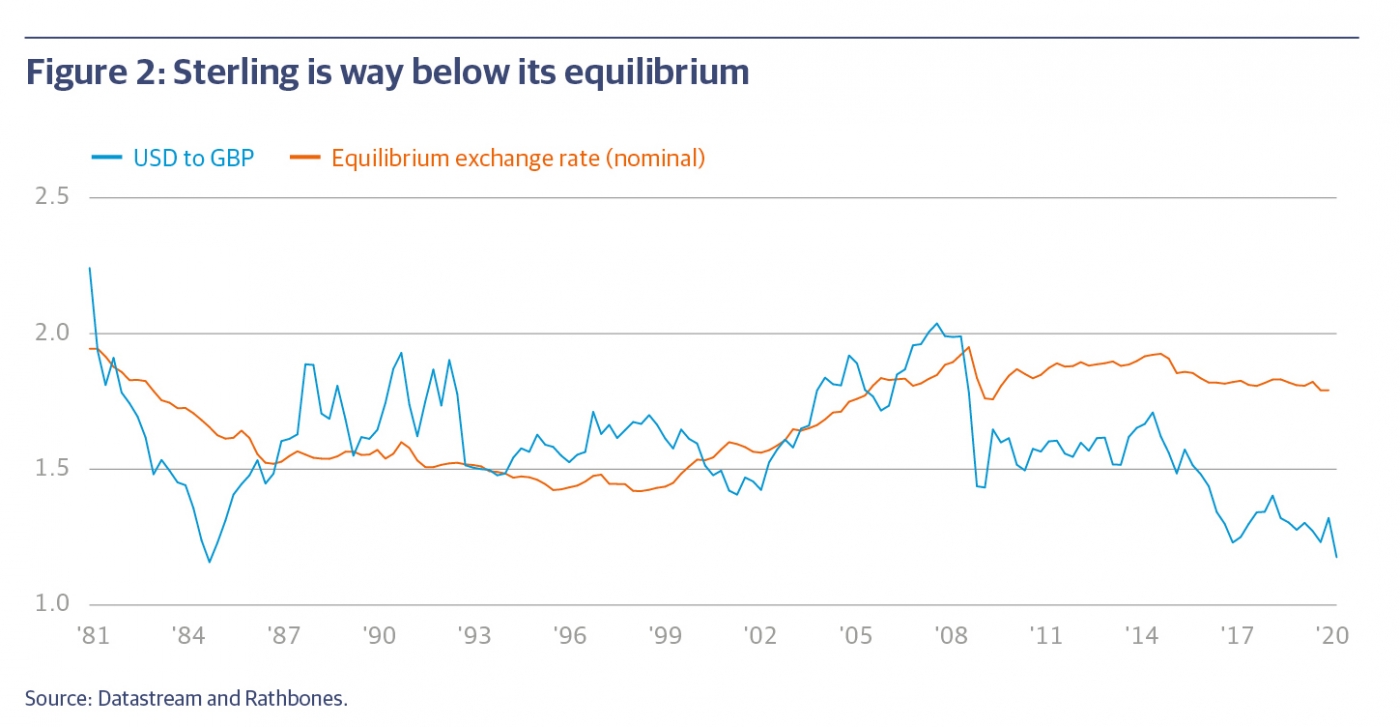

Not a sterling performance

For UK investors, the steep drop in sterling in response to the pandemic may be worrisome. Why has the UK currency reacted so badly, given the rapid and robust response of our policymakers? First of all, sterling is highly cyclical – when markets are in ‘risk-off mode’, sterling falls. The flight to safety has been extreme, and it’s possible we will see sterling fall further.

According to economic theory, exchanges rates follow interest rate differentials (in other words, investors tend to prefer currencies with higher yields). But we wouldn’t bother with interest rate expectations at the moment. Exchange rates follow interest rate differentials, until they don’t. And when they don’t, they really don’t – as is the case today (particularly sterling versus the dollar). Longer term, sterling is way below its equilibrium exchange rate (defined by long-term economic variables such as relative productivity or prices) and we can’t see why the pandemic would do more permanent damage to the UK than other economies. The UK doesn’t have outsized exposures to travel and tourism, or oil exports, and its financial sector is among the best capitalised.

Beware the dash for trash

When the recovery does arrive, there will be a ‘dash for trash’ at some point. We think it would be a big mistake to try to position for that ahead of time, and we hold to our firm belief that in a growth-scarce world, the best place continues to be in quality companies with good growth potential. The literature on the aftermath of natural disasters is interesting: there can be positive economic effects, as more savings are channelled to more productive investments in growth technologies that may ameliorate the consequences of the next disaster. Again, we believe this would benefit many growth companies.