Article last updated 25 November 2025.

|

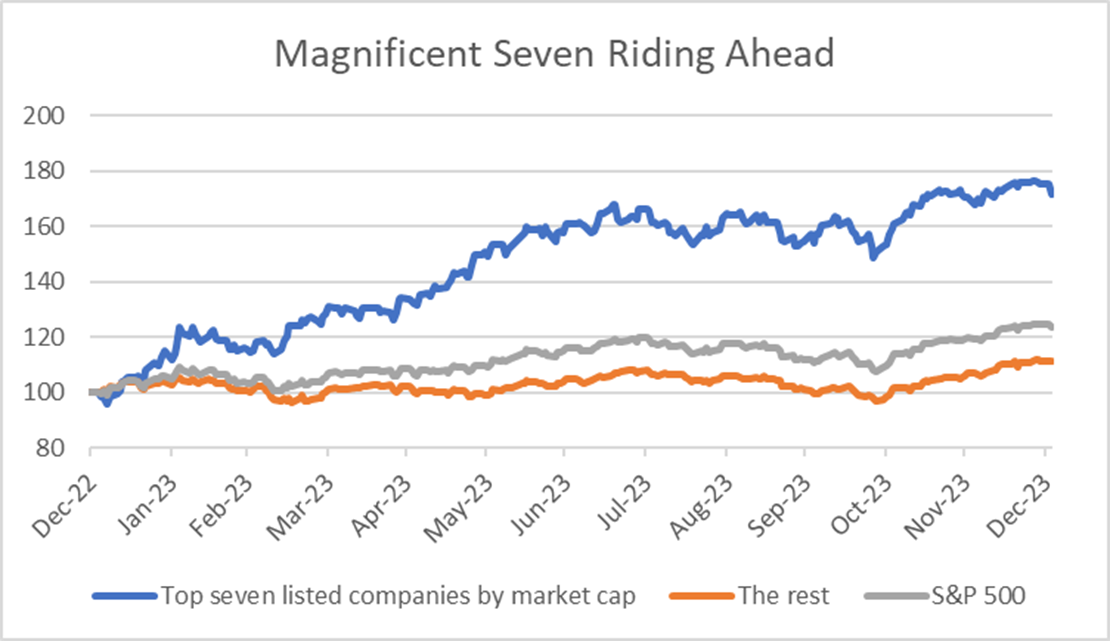

Figure 1:

Source: Refinitiv, Rathbones; December 2022=100, as at 2 January 2024 |

This elite group shares a common thread — they embody the seemingly unstoppable rise of the technology sector, although a less charitable view might put Tesla with the traditional carmakers rather than whizzy software developers.

But there’s an important context to their stellar performance. In many ways, it was a rebound from a disastrous 2022, when they were collectively down a not-so-magnificent 40%. The ‘Mag 7’ accounted for almost as much of the S&P 500’s decline that year as they did the gains in 2023.

They haven’t been the only protagonists in the tech sector’s recent success story either. Oracle, Adobe, Booking Holdings, and even UK-listed Sage have also delivered impressive returns. The pivotal question for investors is not what is driving the Magnificent Seven, but what explains the success of the tech sector in general?

No doubt some of the gains this year have been fuelled by hype around the potential for generative AI (exemplified by ChatGPT). But we believe the broader conditions favouring technology companies will persist, including high returns on capital and structurally advantageous business models, and they will remain an important driver of equity returns. It doesn’t have to be limited to the Magnificent Seven, but we expect more sequels from this band of superheroes.

But this doesn’t rule out a place for bonds in charity portfolios seeking long-term growth. In a huge shift from the pre-COVID norms, there is now a new interest rate regime…

Higher for longer

This snappy phrase can obscure as much as it illuminates. Higher than what? How much higher, and for how much longer? The exact answers to these questions matter a lot for investors.

We agree that interest rates are likely to be higher over the next decade than they were during the 2010s. Several of the factors that pushed down inflation and interest rates in recent decades have now either faded or even shifted into reverse. They include globalisation, fiscal austerity and the need to rebuild household finances after the global financial crisis.

We think the consequences will include greater volatility in inflation and a higher average level of interest rates over the coming decade. In other words, a return to historic norms – over centuries of data the 2010s stand out as an anomaly, with the lowest rates on record.

Markets may be right that rates will stay higher than they did in the 2010s, but wrong about by how much. By historical standards, investors are still pricing in a fairly gentle path of rate cuts. That may prove correct, but we still think there’s a risk that rates fall faster than markets expect if the economic outlook worsens.

And in any case, we know that gilts typically perform well from a few months before the first rate cut until a number of months after it. On top of that, yields are starting from a higher, and therefore more attractive, point than they have for some time. This gives us a greater margin for error. Even if interest rates come down more slowly than we expect, we may still achieve a moderate return from the yield alone.

But with more than half of the world’s population set to go to the ballot box in 2024, will politics drive the markets in what The Economist has called the biggest election year in history?

Election fever

We’ll be keeping a close eye on two contests that may be causing investors angst — the US Presidential election in November and UK election, which must take place by the end of January 2025. Governments on both sides of the Atlantic are in a tough spot, the UK Conservative Party in particular.

Election analysis can be clouded by partisanship and emotion. So as investors, we aim to take a dispassionate view by focusing on the fundamentals that matter most to markets. We can take some comfort from history – our analysis of past elections suggests they rarely change market trends, which are typically determined by factors outside a government’s control (like changes in the global economy or interest rates). In other words, we shouldn’t lose sight of the bigger picture.

For example, plenty of commentary ahead of Trump’s 2016 win suggested markets might react badly given his divisiveness, unpredictability and stances on various social issues. However, no such meltdown materialised.

Political parties evolve, so looking to past cycles is limited. It makes more sense to assess each election on its own merits, comparing party plans on the key issues that matter to investors. We’ll have much more to say as elections approach and we learn more about policy plans, but a few things stand out already.

One surprising observation is the degree of similarity between the opposing parties in both the UK and US on key economic issues. Environmental policy (more on this further down) is one area of clear divergence on both sides of the Atlantic, while a second Trump presidency could have consequences for markets in the areas of foreign policy and the health of political institutions.

History suggests markets look through even the most dramatic political events, provided their direct economic implications are limited.

Against the backdrop of clear divergence on environmental policy between the two main political parties in the UK and US, we take a look at the necessity of energy market reforms to enable the transition to clean energy…

Reflecting on renewables

Over two years ago the cost of renewable power generation fell below the cheapest fossil fuel option. New renewable electricity generation installations continued apace in 2023 and are expected to in 2024. Yet renewable energy stocks endured another torrid year in 2023.

Because renewable energy companies typically agree long-term contracts and fix the price at which they will sell energy before proceeding to develop projects, they were hit especially hard as the Bank of England and other major central banks jacked up interest rates at a record pace.

To achieve commitments to net zero carbon emissions by 2050, there needs to be a proliferation of renewable energy infrastructure across the globe over the coming decades. The policy environment will need to be as supportive as possible.

With this in mind, Rathbones has made energy market reform a priority area for our stewardship activities in 2024. We intend to engage closely with whichever political party is in power following the next general election.

With so much uncertainty and risk out there, we finish on a positive note. As all past economic downturns come and go, so too will this one. In fact, the dawn of recovery looks closer as we begin a new year…

Return of the bull

At the moment it still makes sense to have a cautious investment stance, but as we see recovery more clearly approaching we can begin to prepare for it.

We’ve identified several triggers for turning more definitively positive on the outlook, out of which we think two would be sufficient for a market recovery. One of them, an end to US interest rate increases, seems likely to have happened. A second, a bottoming out in leading global economic indicators, looks likely to happen soon.

The US has made significant progress in bringing down inflation. There’s also evidence that more disinflation is on the way. Therefore, it seems likely that the US Federal Reserve has finished raising rates.

Our own global leading economic indicator has stabilised amid continued resilience in the US economy. Yet we’re not confident it has bottomed out. The latest business surveys point to the eurozone and UK economies contracting, while China’s housing market remains in a deep downturn with only limited policy support. There are also several reasons to expect the recent strength of the US economy to fade.

While we wait for a more definitive recovery to signal the ascendency of the ‘bulls’ over the ‘bears’, what can we do to prepare for the time when this second condition is met, and we turn more positive? Some parts of the global markets that would tend to do well in an economic rebound are looking cheap. They include smaller companies, sectors that are more dependent on broad economic strength and economically sensitive regions like developing markets.

However, we don’t think this alone is a good reason to add more of them to portfolios — they could well get cheaper, given the continued risks to the economic outlook. Valuations alone have been a poor tool for timing entry points in the past.

But we’re ready with our wish list.

If you'd like to read the full report, please click here.