Article last updated 13 February 2026.

Article last updated 13 February 2026.

Important information

This information is based on our understanding of HMRC tax rules in the UK. Tax treatment depends on individual circumstances which could change.

![]()

Seek advice early

These changes cut across valuation, tax, legal documents, and liquidity — a joined‑up accountant/solicitor/financial planner conversation now is better than a rushed fix later.

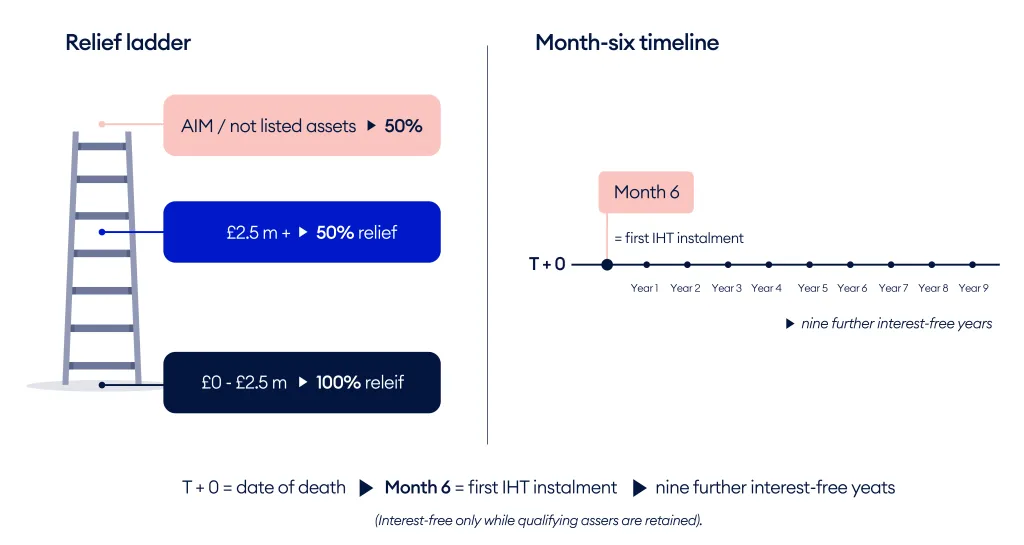

A £2.5m allowance will also apply to the combined value of relievable agricultural and business property in trusts, with detailed rules on how it applies across trusts and settlements (including transitional rules).

Neither BPR nor APR (at any level) is available for otherwise qualifying investments held inside pension funds.

Index linking: the £2.5m limit is planned to remain fixed until 5 April 2031, with CPI index-linking proposed from 6 April 2031 (subject to confirmation).

IHT on qualifying assets can still be paid in ten annual instalments; the first falls due by month six after death. Interest free treatment continues only while the asset retains qualifying status. It has been clarified that the instalment facility applies regardless of whether the asset qualifies for 100% relief (up to £2.5m cap) or 50% relief on all value.

Part of the value that previously expected 100% relief may now sit at 50% relief (effective 20% IHT on that slice). Valuation principles, including control discounts, are unchanged - but funding becomes the new pressure point.

Transferability helps, but misalignment can still lead to under-use of the combined £5m 100% relief and create avoidable liquidity issues on the second death.

From April 2026 these holdings move to 50% relief. That can be fine, but it makes suitability, volatility and liquidity even more central, because a tax-driven strategy can still leave a real cash bill.

Where 100% relief is capped, trustees must factor the cap into exit-charge calculations and executors must plan for a month-six payment, or instalments, where 50% relief leaves tax to fund.

![]()

Allowance mapping (one page, joined up)

A simple grid across client/spouse/civil partner trusts showing: £2.5m @ 100% used, value at 50% relief, including AIM/not listed, and the resulting tax and liquidity requirement.

![]()

Ownership and documents alignment (so the plan works in real life)

Where appropriate, rebalance qualifying holdings so each spouse is positioned to use or transfer a full allowance, regardless of order of death. Refresh wills/letters of wishes and align shareholder/cross-option documents where business continuity matters.

![]()

AIM / “not listed” audit (risk, liquidity and timing – not just tax)

Quantify AIM exposure and the post-April 2026 IHT position. Where suitable, explore alternatives. Managing two-year qualification periods and the practical timing risks around reinvestment.

![]()

“Month-six liquidity” by design

Appropriate whole-of-life cover written in trust can create cash for the month-six deadline and/or fund instalments, reducing forced-sale risk. (Any insurance solution must be assessed for suitability and affordability.)

![]()

Trust readiness and record-keeping

Ensure trust records correctly track the settlor’s use of the £2.5m allowance, including seven-year tracking where relevant, and monitor qualifying conditions to protect relief and the interest-free instalment facility where qualifying assets are held in trust.

If you have a client where APR/BPR value may exceed £2.5m (or where AIM / “not listed” exposure is part of the plan), we can help with a short, no-obligation triage call to sense-check the position and identify the most useful next step.

Bring one anonymised fact pattern (asset mix, ownership, approximate values, and any trusts) and we’ll come back with a simple action outline: allowance use, month-six liquidity considerations, and where legal/tax documentation might need aligning - with your firm remaining central to the tax/legal advice.

|

Before April 2026 |

After April 2026 |

|

| Qualifying shares | £7,000,000 fully relieved ⇒ £0 IHT | £5,000,000 at 100% relief (2 × £2.5m) ⇒ £0 IHT; remaining £2,000,000 at 50% relief ⇒ £400,000 IHT |

| Other assets (RNRB not available: estate >£2m) | (£5,000,000 – £650,000) × 40% = £1,740,000 | £1,740,000 |

| Total IHT (second death) | £1,740,000 | £2,140,000 |

The relief still helps, but above the allowance, the important job becomes quantifying the exposed slice and designing month-six/instalments liquidity.

From 6 April 2026, 100% relief is capped at £2.5m per individual across APR/BPR, with 50% relief above that cap — and 50% relief on all AIM / “not listed” holdings.

For your affected clients, the practical priority is to:

![]()

Where clients use (or are considering) BPR‑qualifying investments, suitability, investment risk and liquidity must remain central — and clients should take personal advice before acting.