Looking for someone to create an investment portfolio for you?

Article last updated 7 May 2026.

|

Quick take

|

In April, a small island off the coast of mainland China reached an impressive milestone by beating a somewhat larger island off the coast of Europe. Taiwan’s stock market surpassed the UK’s, by attaining a total market cap of $4.13trn, thanks to the rise (above $2trn) of Taiwan Semiconductor Manufacturing Company (TSMC), which produces around 90% of the world’s high-end chips.

This highlights something we’ve long observed: the label of emerging markets (EMs) often reflects a country’s historical status as up-and-coming rather than its importance in the world today. Coined by the World Bank in 1981, the term has stuck.

It tended to describe countries that offered considerable potential but didn’t enjoy the governance or standard of living of developed countries. But much has changed since then. Many readers may well, on their travels, have experienced better conditions in socalled emerging economies than at home in developed Western economies.

However, the compilers of global equity and bond indices have been surprisingly conservative. When it comes to indices run by data provider MSCI, only two countries have crossed over to developed status in almost five decades: Portugal and Israel. No such promotion for Taiwan.

At the end of March, MSCI’s EM equities index was dominated by Asian countries. China led the pack with a 25.5% weighting, followed by Taiwan (22.5%), South Korea (15.5%), India (12.5%), and Brazil (5%). On the African continent, only South Africa and Egypt are classified as EMs. The rest are merely in the ‘frontier’ niche investment category.

A change of emphasis

This century, EMs have had two sustained periods of outperformance. The first followed China’s 2001 accession to the World Trade Organisation. By unlocking the Middle Kingdom’s potential as a mammoth exporter, this event triggered enormous investment in infrastructure and manufacturing. During this period, ending with the 2008 global financial crisis, banks and resource stocks dominated EM indices. The second followed China’s massive stimulus in response to the crisis. But this didn’t last long, and was well and truly over by the time China devalued its currency in 2015. The worst period of performance came after China punctured its speculative real estate bubble in 2020.

The phoenix rises

EMs have seen a reversal of fortunes over the past year or so.

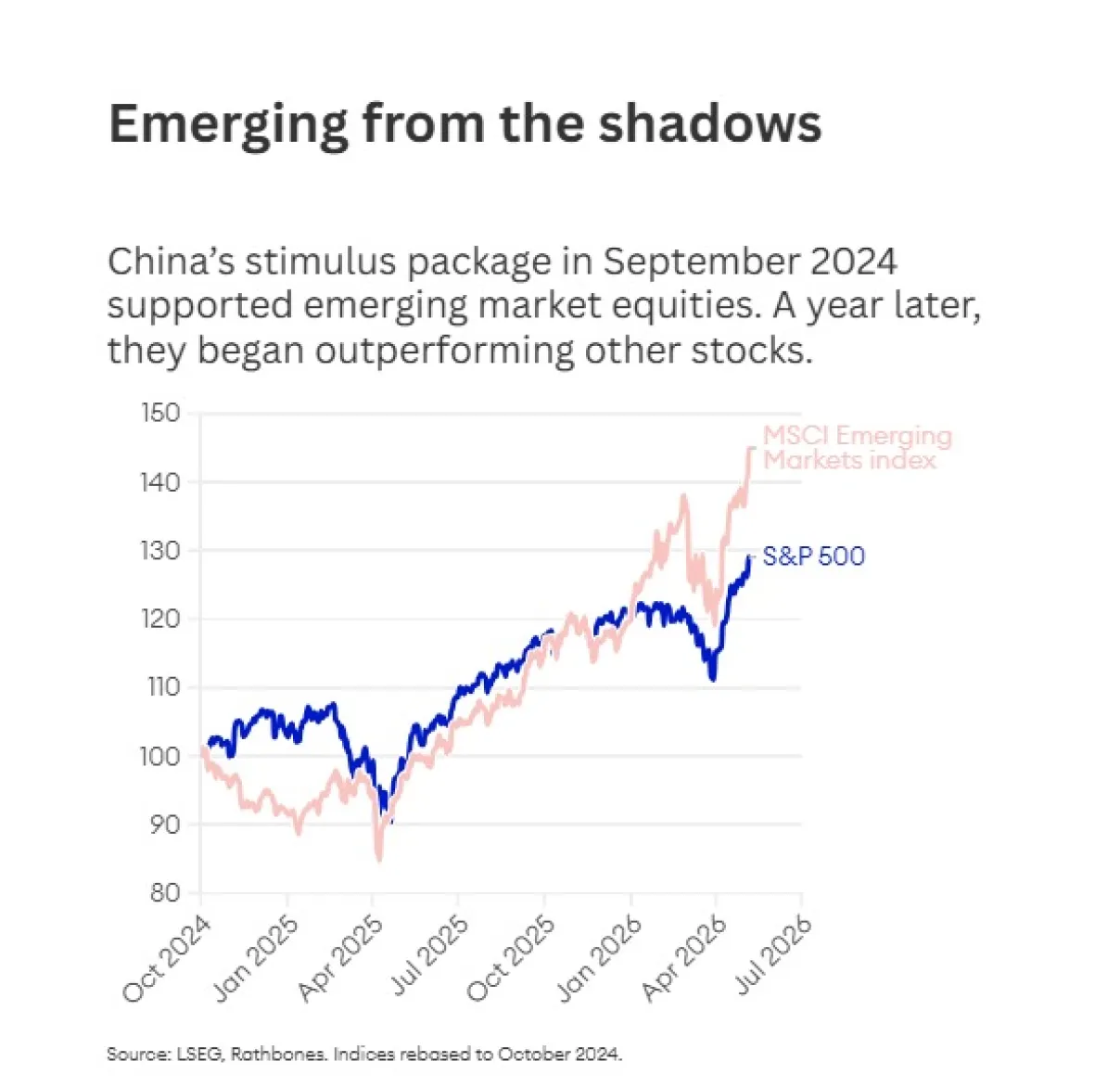

The major turning point came when China announced an expansive stimulus package in September 2024. This provided support to the market, paving the way for a more sustained rise over the past year. Another tailwind is dollar weakness. That helps EM companies because their dollar-based corporate and state borrowing becomes easier to finance.

The most recent strong driver of returns, and in many ways the most exciting, is the extraordinary rise of companies exposed to the AI revolution. TSMC encapsulates this: its chips are a crucial component of data centres. TSMC is by far the biggest company in the MSCI EM index, accounting for 13.3% of its market cap. The next biggest are Samsung (5.1%), Tencent (3.9%), SK Hynix (2.8%), and Alibaba (2.6%).

Like TSMC, South Korea’s Samsung and SK Hynix are in the chip business – specifically, the memory chips needed to power the large language models used by chatbots. China’s Tencent and Alibaba are technology and consumer platform companies, but both embed AI in their offering. Both also have cloud businesses that benefit from the huge demand for computing power needed by AI. And having lost ground in March on fears that markets might have got ahead of themselves, EM tech stocks enjoyed an excellent April.

Not your father’s emerging markets

The result of this structural shift is that Technology is now by far the largest sector in the MSCI EM Index, accounting for 31.8%. If we add Tencent and Alibaba, which are classified under Communications Services and Consumer Discretionary, respectively, this figure rises to 38.3%. When EMs were in full flow in 2007, Technology was only 13.2%. This change is mirrored in MSCI World.

Due to this change, the performance of EM equity indices is often much more correlated with the US’s tech-heavy Nasdaq index than before. At the overarching level, this makes EM less of a diversifier than in the past. But its tech companies tend to be more attractively valued than those in the rest of the world. This offers rewards for investors willing to endure greater political risk.

Scars and resilience

Since China’s economic stimulus began, EM equities has been the best-performing of the major regional asset classes, posting a total return, by late April, of 45.5%, vs 28.6% for the MSCI All Country World Index. This period has encompassed both US President Donald Trump’s ‘liberation day’ tariffs and the war in Iran. That suggests EMs are more resilient than in the past. It helps that corporate governance has improved greatly over the years. Moreover, scarred by past crises, EM governments and central banks have improved their management of both currency and inflation risk.

When it comes to currencies, the dollar pegs that led to over-borrowing and subsequent collapses have, since the late 1990s, largely been replaced by floating exchange rates that provide a safety valve. These pegs fixed the value of a country’s currency against the US dollar. Past experience of higher inflation drove many central banks to be quicker off the mark in raising interest rates in 2021–22. That means they weathered that storm better and still have some firepower to cut rates.

Hidden treasures

In the short term, many EMs face uncertainty as the Iran conflict creates shortages of key commodities, such as oil, gas, and fertiliser. Further obstacles to global trade, born of politics, environmentalism or industrial protection, could also create a headwind. Climate change might herald upheaval, too.

Positively, prudent past monetary policy leaves many EMs positioned well to withstand incipient inflationary pressures. And GDP growth tends to be higher than in the developed world. That hasn’t guaranteed outperformance in the past, but it does help to be a company selling into an expanding economy. Moreover, improved corporate governance could mean higher returns on capital.

As well as the tech story, specialist EM managers often have greater scope to beat benchmarks than managers in some bigger developed markets. That’s because each individual market has fewer managers looking for undervalued companies – which, once found, are no longer undervalued. As well as phoenixes, emerging markets may offer hidden treasures.