Looking for someone to create an investment portfolio for you?

Article last updated 13 May 2026.

Quick take• Oil pricing suggests easing tensions – but uncertainty is keeping investors cautious. |

All missives currently begin with the caveat “at the time of writing”. I’ve noticed that many podcasters now ‘date stamp’ their conversations too. As I outlined in the latest Monthly Digest, the world in which we awake these days is not necessarily going to be the same one in which we went to bed. The main source of current uncertainty remains the situation in the Middle East, but domestic issues such as the travails of the Labour Party are influential. And if you turn in without checking the latest results from Wall Street’s biggest companies, then you are missing some late night fireworks too.

Where is the love?

The war in Iran remains ‘top of mind’ for now, mainly thanks to its influence on the price of oil and gas and related commodities. If you want to take delivery of a barrel of oil today, it will cost you around $108. But if you are happy to wait until December, it will be $88, at least based on futures prices. The market is signalling that some sort of agreement can be reached that will allow tankers to navigate the Strait of Hormuz again. The collective wisdom of the crowd is often (but certainly not always, in retrospect!) the best guide to the future.

Even so, the risk of a more negative outcome still restrains us from increasing equity weightings in balanced portfolios. That’s been a bit frustrating as markets have continued to rise but represents, for us, the right balance of risk and reward. As written about previously, the effects of higher commodity prices take a while to feed through and the world is still working its way through inventories. Should they run out, more stress will become evident.

In reality, we would hardly expect Iran and the US to kiss and make up. The future price of oil is going to reflect a degree of uncertainty as well as the need to rebuild the stockpiles that have been drawn down, amounting to around a billion barrels by now. We are also concerned that if there is no final agreement concerning Iran’s nuclear capabilities, then the issue might rear its head again sooner, not later. Indeed, one of our geopolitical analysis providers fears that President Trump might kick the can no further down the road than November’s mid-term elections before re-escalating. Suffice to say that we are constantly re-evaluating the situation.

Better to have loved and lost?

Behavioural science provides some very interesting insights into investing. Probably more than ever, given the cacophony of news and opinions that we are assailed with daily. As I often point out, the negative headlines are the ones that people listen to the most. And doomsayers and bear market proponents also seems to garner more than their fair share. Indeed, I suspect someone in a newsroom somewhere has run the numbers on the increased levels of reader/viewer engagement when the world “crash” is introduced.

Three closely related theories are relevant to how one might consider one’s biases: prospect theory, loss aversion and the endowment effect. Prospect theory, developed by Daniel Kahneman and Amos Tversky, concerns humans’ attitude to the risk of loss against the potential reward of gain. They value gains and losses differently. The desire to avoid losses, or potential losses, outweighs the potential for gain. Within that theory, loss aversion posits that the negative emotional impact of loss is around twice the benefit of a gain.

The endowment effect is somewhat different. It holds that people value an object more because they own it. The classic study was that of students who were offered a mug and asked how much they would be prepared to pay for it. They were then given the mug for nothing but later asked how much they would be prepared to sell it for. The mere act of (fleeting) ownership meant that the average asking price was raised.

Think what this means for investing. If you are always worried about the market going down, you will never have sufficient confidence to invest enough to meet your objectives. And this is in a world where the long-term returns from equities empirically outweigh the possible loss of capital. That’s not to say that there are no times when it’s advisable to sell (or at least trim the sails). Often, the best time to sell is when a stock or market has peaked and is turning down. But this is where prospect theory kicks in, overcoming loss aversion. The owner holds out for last week’s price, rather than focusing on the much larger gains that could still be banked.

Today, we have a potent narrative surrounding artificial intelligence combined with what is turning out to be one of the strongest corporate reporting seasons on record (notably for US companies). Not only that, but market earnings estimates for the whole of 2026 and 2027 are still rising. Of course, given the potential for events in the Middle East to turn against us, these estimates might not be sustainable, but it feels wrong to stand in the way of such positive momentum. It makes more sense to give back some future gains than never to make the gains in the first place.

Love’s Labour’s lost

Shakespeare’s play of this title was a comedy. That hardly seems appropriate to the mauling experienced by the Labour Party at last week’s local and mayoral elections. Indeed, I find myself living in a borough (Hackney) that has just returned the UK’s first ever directly elected Green Party mayor. It looks premature to be dusting off our general election playbook, but we certainly need to keep an eye on developments within the Labour Party. It’s a widely held opinion that the departure of Prime Minister Keir Starmer (accompanied, inevitably, by Chancellor Rachel Reeves) would be viewed as a destabilising market event, likely to take policy further to the left.

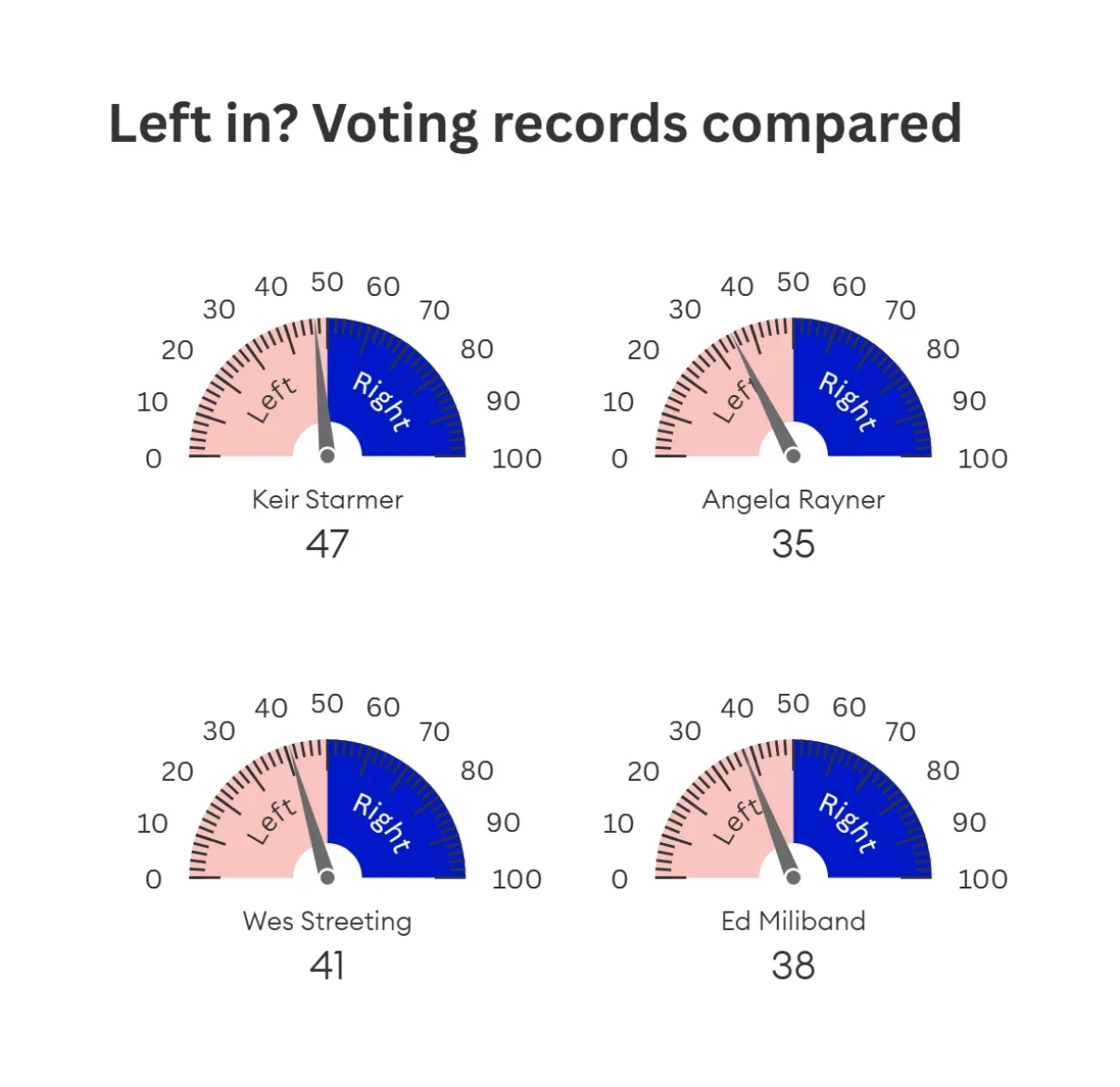

The Polymarket betting site (a credible reflection of sentiment) shows a 46% probability of Starmer being out by the end of June. It was as low as 17% on Monday evening and as high as 65% on Tuesday morning. This is a volatile situation. The odds for a new leader (and PM) favour current Mayor of Manchester Andy Burnham, followed by Wes Streeting, the more centrist Health Secretary. Former Housing Secretary Angela Rayner is running third, followed by Energy Secretary and former party leader Ed Milliband.

The reaction to the election results on Friday was relatively muted. UK government bonds outperformed a little and sterling rose in value because the results were no worse than expected. This reaction may also have reflected that fact that the Green Party (now viewed as the most left-wing major party) didn’t really surprise to the upside.

The emergence of a potential ‘stalking horse’ Labour leadership candidate, Catherine West, over the weekend took some of the gloss off on Monday morning, and market sentiment deteriorated throughout that day following various resignations and more calls for Starmer to step aside. On Tuesday morning, investors continued to sell gilts and the pound in response to the increasing risk of destabilisation. These asset classes tend to be the most reliable weathervanes when it comes to evaluating political risk. Longer-dated gilt yields are making multi-decade highs, increasing the cost of debt when the fiscal situation is already testing. The pound remains at the upper end of its trade-weighted post-Brexit trading range, suggesting no imminent crisis. But the situation is fragile.

There’s little to suggest that an even more disruptive general election is imminent. With a huge Labour majority, it’s improbable that a vote of no confidence could succeed. Especially when many current Labour MPs are at risk of losing their seats to Reform or Green Party candidates. And even if there was a general election, neither party is close to achieving an overall Parliamentary majority based on current polls – and that’s before we take potential tactical voting into account. We’ll definitely be publishing more thoughts on how this might all play out, but we could be waiting as long as three years for a general election.

Returning to Shakespeare’s play, it follows three lords who swear an oath to fast and avoid women for three years to focus on their studies. Maybe Labour’s leaders should similarly focus on getting on with doing a good job. The characters in the play are quickly led astray by the arrival of attractive ladies. At least hilarity ensues. The more politicians lose focus on their responsibilities to the electorate, the more it turns from a love story into a tragedy.

Streeting's voting record is only slightly left of Starmer's - but other likely candidates are further to the left