AI is reshaping media, music, and copyright, giving companies with valuable content libraries new licensing opportunities. But AI poses risks for investors too.

Article last updated 11 May 2026.

Quick take

|

An opinion piece in the Financial Times earlier this year struck a chord with me. The author, Armen Sarkissian, is an arresting combination of two things: a former President of Armenia and a theoretical physicist.

Sarkissian postulated a world in which uncertainty has become the norm. He drew on his experience to describe a “quantum” world in which “outcomes are probabilistic rather than deterministic” – essentially, it’s much harder to know what will happen, even if you know what the inputs are. And in this world, “observation itself alters reality.”

Investors have actually long dealt in uncertainty, weighing risk against opportunity in constructing portfolios. But Sarkissian’s point was that the inputs which we have to evaluate when making these decisions, especially in politics, are increasingly uncertain. He gave the example of Greenland. If the norm that no Nato power ever threatens to take the territory of another is dissolved, this suggests we’re now in a world that’s much harder to understand and predict.

Sarkissian further invoked the work of Anglo-Polish sociologist Zygmunt Bauman, who described our current condition as “liquid modernity”. Ours is a world in which we can go to bed in one political reality and wake up in another; a world in which structures melt faster than they can be rebuilt. When politics is so polarised, news headlines are so sensational, and it’s not unusual to witness share prices move up or down more than 10% in a single trading session, I find this framework useful. But regardless of the uncertainty, we shouldn’t be scared out of sensible long-term investments.

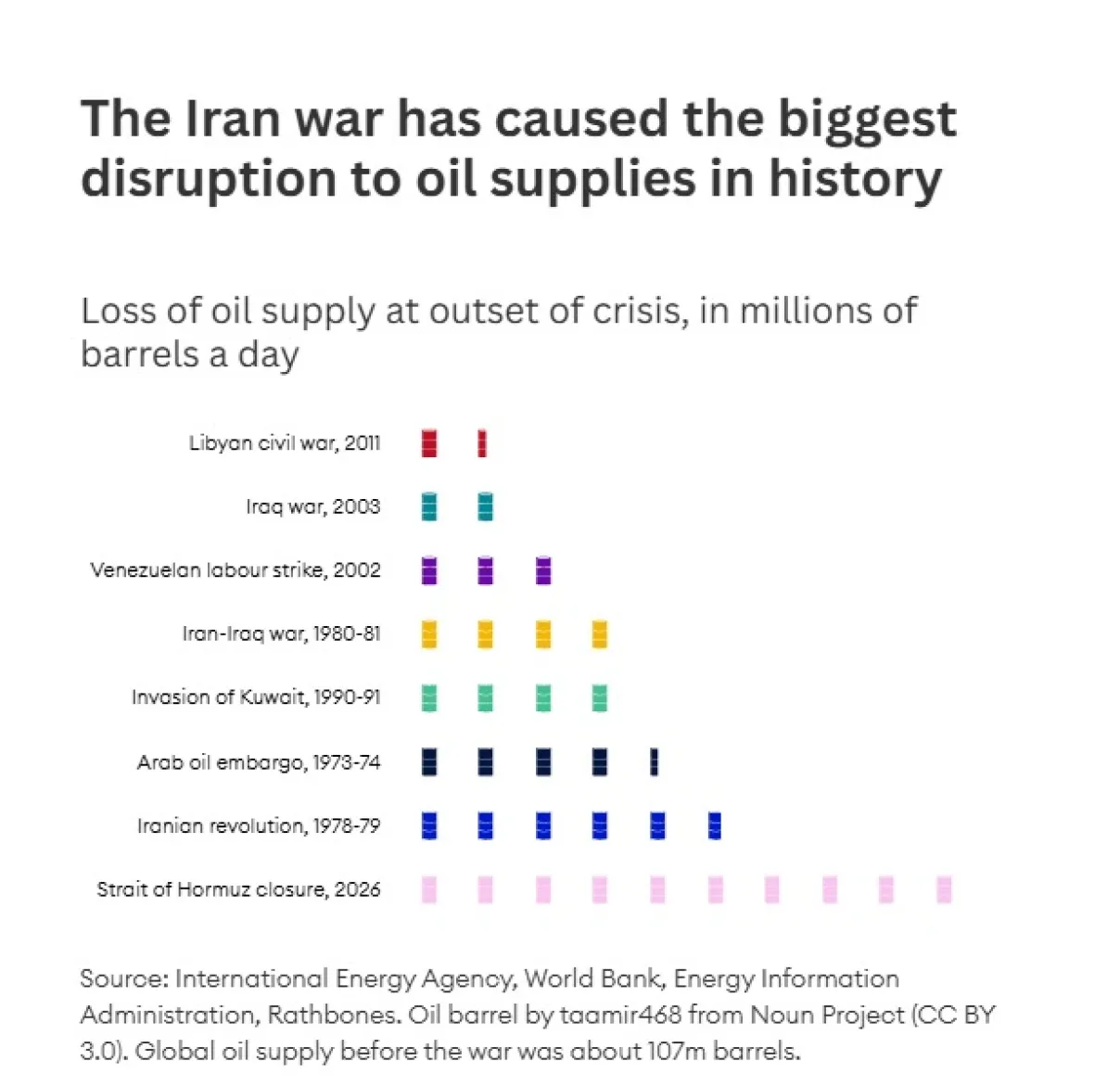

Ripples from the Gulf

Our stance throughout the Iran conflict has been that the current situation is not to anyone’s benefit, and one has to have a modicum of faith that we’re not headed into some form of mutually assured destruction. With this in mind, we haven’t reduced overall market exposure, especially as any further rallies could be quite sharp and immediate on any firm news of a resolution. We’ve already seen that happen a couple of times.

As May opens, we’re encouraged that the US and Iran appear still to be in negotiations, with the ceasefire still on. But it’s not abundantly clear what either side will settle on as being sufficient to declare victory. For Iran this could be a lifting of sanctions and an acceptance that the current leadership can remain – and to generate revenue from ships passing through the Strait of Hormuz. This could potentially be achieved under the guise of reparations.

For the US the key objective appears to be some sort of oversight of Iran's nuclear capabilities, plus a commitment not to produce nuclear weapons. For now, these seem the key sticking points. As for the timing of an agreement, Iran is probably prepared to show more patience than the US – and that strengthens its ability to argue for better terms. For US President Donald Trump, the clock is ticking on the countdown to November’s mid-term Congressional elections. He’ll want to put the economy on a strong footing to maximise the Republican vote. But don’t be surprised if we see further escalation before the denouement.

There are plenty of potential risks in this situation. And they may well increase exponentially, if the Strait of Hormuz remains closed. We’re now at the point when cargoes of oil and other vital commodities that had left the Gulf before the hostilities have reached their destinations – and there are few cargoes left to come. We could soon be witnessing not just higher prices but also actual shortages. That could have a greater negative economic effect.

Although the oil price tends to dominate headlines, other commodities in short supply because of the Strait’s closure include urea, ammonia, and sulphur, all of which are key components of fertiliser. This is just as the northern hemisphere’s spring planting begins. Butane and propane, which are also affected, are important fuels in Asia and Africa, primarily for cooking. Helium is critical for cooling semiconductor manufacturing equipment and MRI scanners.

Moreover, a quarter of the world's supply of aluminium, an important lightweight metal used for construction, transport and packaging, originates in the Middle East. It accounts for about 10% of a solar panel’s weight, so the lack of availability will hinder the transition to greener energy. On the same theme, a typical 3-megawatt wind turbine contains roughly 3 tonnes of aluminium.

UK consumers have already experienced higher petrol and diesel prices at the pump – and higher airfares. But the impact of Middle Eastern events might not be fully felt until holiday flights are cancelled more frequently, as jet fuel is rationed. The global number of flights has already fallen by around 3%. A decent chunk of this is flights beginning in or routed through the Middle East.

Leaning towards de-escalation

You might well ask why we’re not taking a more defensive stance. Our answer: we continue to believe that investors, and therefore financial markets, will look through negative effects in the short term, as long as they expect resolution in the long term.

In thinking about the best course of action, we’ve constructed various scenarios, giving each a numerical probability: what’s the chance it will happen? We still place the greatest weight on de-escalation. That means a re-opening of the Strait of Hormuz, although perhaps only a gradual increase in traffic to previous levels. This might see the price of oil return to $80 a barrel in financial markets, down from above $110 at the moment.

Even so, that will be higher than before the war. This is partly because, having released barrels from their petroleum reserves to ease shortages, governments will need to build them back up again. It’s also because, even after the war, financial markets will continue pricing in a risk premium – an extra amount of dollars for every barrel, because the risk of another bout of severe disruption now looks more likely.

One factor working in investors’ favour, though, is the growth of corporate earnings. With the first-quarter results season now in full flow, it’s clear that many industries entered the period with a good head of steam. Looking further ahead, the current consensus forecasts show very strong growth – almost 20% – in global annual earnings for 2026. That’s largely down to technology, thanks to the capital expenditure on data centres and AI. That said, these estimates depend on the highly uncertain outcome of negotiations between the US and Iran.

Happy in the long term (like Goethe)

For many people, the biggest challenge of the last couple of months may well have been to remain committed to their investments in the face of an almost incessant barrage of negative headlines. Unfortunately, to return to the theme with which I began this essay, we might have to get used to this being ‘business as usual’. To repeat some things we’ve already said this year: we characterise ourselves as investors and not traders; and we continue to recommend that regular savers remain committed to their planned investment schedule. Maybe, in this day and age, a successful investor’s life will feel in retrospect like that of the German writer and polymath Johann Wolfgang von Goethe. When asked about his life he said it had been a happy one but he couldn’t remember a single happy week!