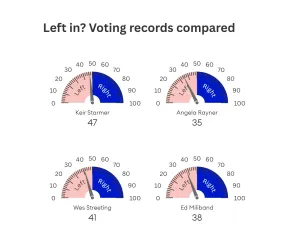

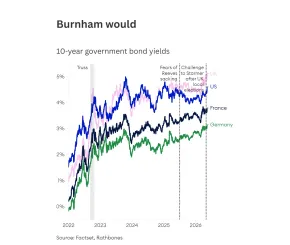

As speculation rises that a left-winger could replace Keir Starmer, UK gilt yields have risen to levels last seen before the financial crisis, bringing renewed focus to inflation, public finances and borrowing costs. Equity markets continue to be supported by earnings growth and AI investment, even as higher yields play a more visible role.

Article last updated 18 May 2026.

Trump 2.0: Market noise, policy changes and what matters for investors

The first year of Trump 2.0 has been a lot. Like a TV soap’s constant twists and side plots that keep you glued to the screen, President Donald Trump has kept the world in thrall every single day. Many despise him, many love him. All should respect his understanding of how to operate in a media-saturated world.

Yet we should be careful of conflating ‘being a good operator’ (i.e. ‘getting things done’) with ‘implementing good policy’. Trump’s record on this is decidedly mixed. He has stripped back many regulations and cut income taxes. But examples of fraud and poor loans are rising along with the government’s huge spending deficits. He has clamped down hard on illegal immigration, but in doing so put the net flow of people into the shining city on the hill into reverse for the first time in at least 50 years. And, most iconically, Trump upended global trade by imposing big and ever-changing tariffs on virtually all imports. This has raised not-inconsequential revenue for the government, but came at the cost of a lot of goodwill from its long-time allies and a big drop in the dollar. And Trump’s reaction to the Supreme Court’s rebuke of his tariffs – essentially finding other tenuous ways to levy taxes that should sit with Congress – has strained the relationship between the branches of the US government.

These are big shifts in the American paradigm that we have all lived through for the past 30, 40 years or more. So what’s the likely effect for investors, and what should we do about it?

Big shock, but it didn't change the upward path for stocks

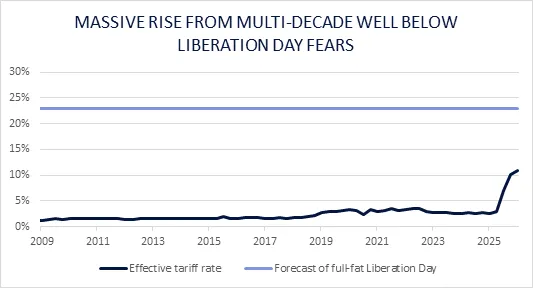

Exactly a year ago, when Trump revealed his oversized placards with reciprocal tariffs for most of the world, virtually everything dropped: global stocks, bonds and the dollar. These new taxes were estimated to raise the average US tariff rate from roughly 2.5% to 23%. Investors worried that it would completely gum up trade, destroy economic growth and send inflation soaring.

This was a scary, risky time. But we thought it wasn’t a time to panic and cut and run. Investing comes with the risk of market falls – it’s the price we pay for better returns in the long run. Often you must stick to your guns to reach those long-term returns. So we assessed our portfolios, gauging which were least likely to be heavily affected, and bought those assets that we thought were on sale – those that were falling simply because everything else was. These included computer chip factory Taiwan Semiconductor Manufacturing Company, top-end chip designer Nvidia, Canadian e-commerce platform Shopify, and German warehouse kit and automation expert Kion. We also bought German smartgrid and electrification specialist Schneider Electric, US universal bank Morgan Stanley and British pharmaceutical firm AstraZeneca. All of these companies operate globally and are leaders in their fields.

We also accelerated the diversification of our government bond holdings. We added some US Treasuries at cheaper prices, but we bought European, Australian and developed Asian sovereigns as well. We have continued to do this in the year since. We have kept our US weightings, however.

Since Liberation Day, the effective US tariff rate rose steadily but remains well below initial forecasts. The Yale Budget Lab thinks it should stay roughly flat to down from here. While US stocks have rebounded strongly, the same can’t be said for the dollar and American government bonds. Both remain significantly cheaper than they were on the eve of Liberation Day.

Source: FRED, Rathbones; quarterly total customs receipts as % of goods imports to the US

What mattered for investors - and what didn't

We didn’t make these decisions because of Trump’s Liberation Day tariff – the upheaval just gave us the opportunity to make these trades more quickly and at better prices. Our plan was based on a longer-term view of how technologies, demographics and policy decisions will affect the world.

Shorter term, we thought the US economy would most likely continue to forge ahead, slower than otherwise but easily avoiding recession. And that Europe – particularly Germany – could see an uptick in growth, supporting the global demand that is what drives corporate profits in the long run. Having said that, we haven’t signed up to the theory that US exceptionalism is coming to an end. The old saying that the US innovates while Europe regulates still holds true. And trade, well, it’s like water: it will find the path of least resistance in no time at all. It’s very difficult to hold back the tide.

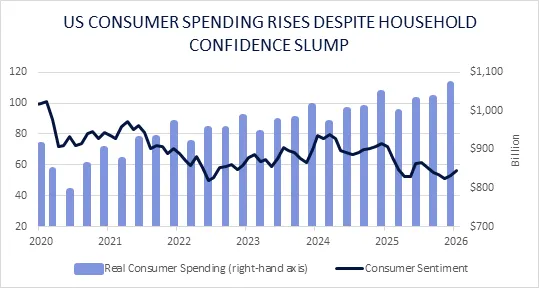

As it happens, that’s broadly what transpired. Global economic growth has dipped yet recession was avoided. Trade routes and supply chains have been rejigged, and inflation didn’t roar higher as some feared. Americans are certainly more downbeat when talking to pollsters, yet that hasn’t stopped them from spending noticeably more.

Source: FactSet, FRED; Uni of Michigan Consumer Sentiment is index level, consumer consumption spending is quarterly inflation-adjusted in 2017 dollars, Jan 2020 to Jan 2026

When Trump is in the White House, we’ve learned to expect uncertainty and a whirlwind of shock decisions and left-field suggestions to keep nations, businesses and the press off balance. In the meantime, Trump and his administration hustle towards their goals. It pays to be aware of these goals and align portfolios to them, as they are the direction of travel for the world’s most powerful office. For all the noise and attention-grabbing headlines, we believe Trump’s team is ultimately looking to achieve these aims:

- Greater energy independence

- Lower bond yields

- Deregulation

- Tax cuts

- Onshoring of key strategic industries

- Reducing overseas tax competition that keeps US profits offshore and untaxed

- Increased access to overseas markets for US companies

- Boosting tariff revenue, thereby lowering government deficits

You can see that the consequences of the Israeli-American war with Iran clash massively with points one and two. We believe this will push Trump to make a deal and de-escalate. Of course, this awful dance is a three-way tango. It’s not enough for the US to want peace; Israel and Iran must agree. This is the biggest risk to markets at present: that Trump has completely lost control of the situation. The effects would be severe: economic growth is just energy with a fancy mask on. That’s why we tend to hold three oil majors (Total, Chevron, Shell) as a hedge against energy shocks. Renewable energy is a critical and growing fuel for global economies, but the world still runs on oil and gas.

Yet even if the energy crisis continues, the long-term dynamics of the world remain in place: people are getting older, government coffers are coming under greater strain, and better technology is the key to doing more with less. We believe the best businesses are the ones that deliver those new tools.

While Trump can create a lot of short-term volatility, I still believe the Constitution is strong enough to keep him in check. The Founding Fathers were very concerned that a Trump-like figure could one day get into the White House, which is why they created the nation’s system of checks and balances.

America is bigger and more powerful than one man. It is successful and prosperous because it’s open and free, and allows its citizens to dream big and win big – or fail big, learn and start again. We will start to worry about the US only when most Americans no longer believe in that simple premise.

This is a financial promotion relating to a particular fund range. This information should not be taken as investment advice or a recommendation. When you invest your capital is at risk and you could lose some or all of your investment.