As higher rates, tougher taxes, and weak wage growth bite, UK property looks less like a one-way bet. A diversified portfolio may offer a stronger path to returns.

Article last updated 24 June 2026.

Quick take• Higher gilt yields underline the challenges facing government finances and future policy decisions. |

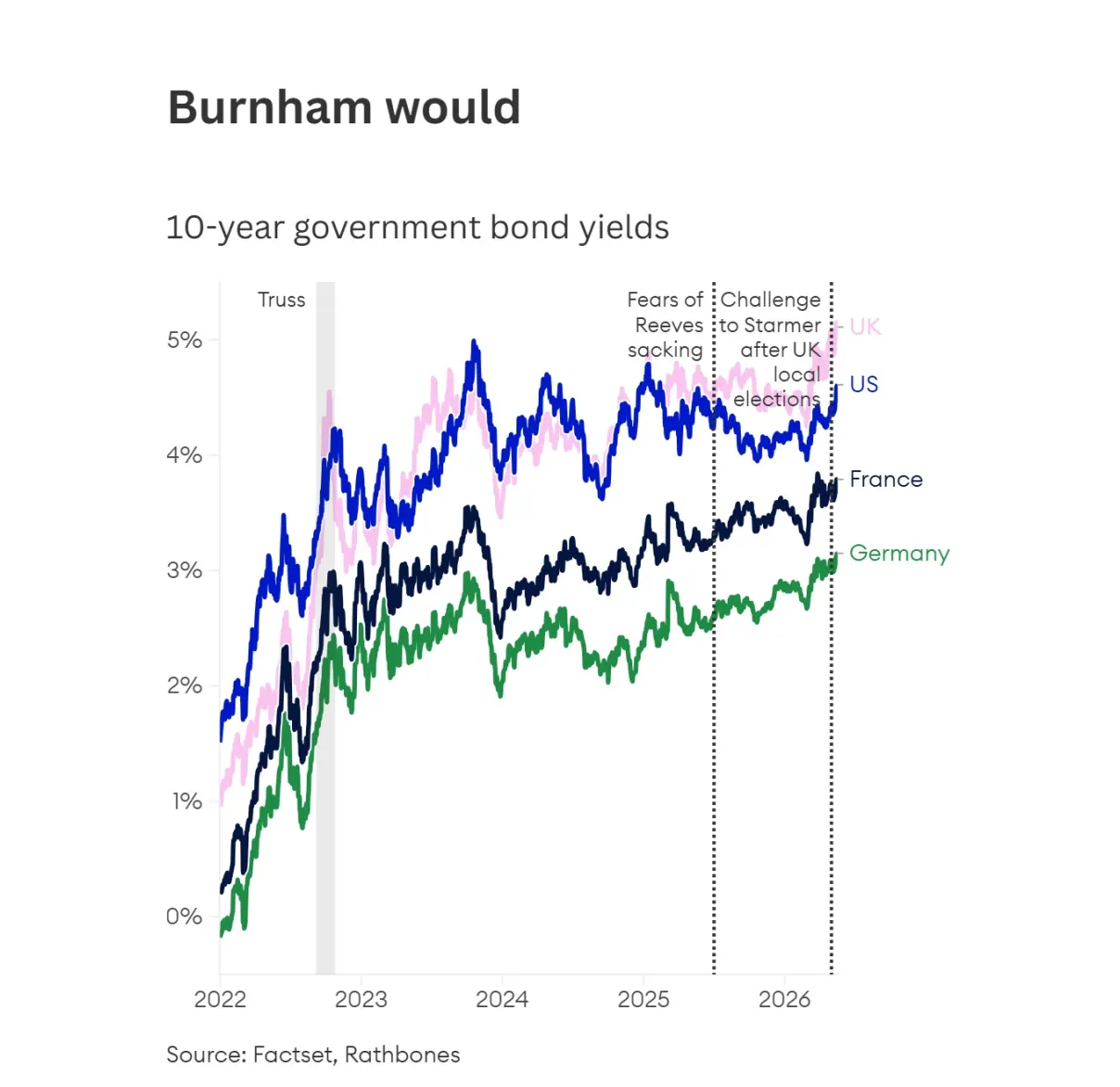

Even those with no great interest in investment matters will have noticed the headlines over the last week concerning the travails of the UK’s government bond market. You’ll likely be aware that bond yields have reached their highest level since 2008. And that the country’s finances are in a worse state than in the aftermath of 2022’s ‘mini-Budget’ during Liz Truss’s short premiership.

A gilt with a 30-year maturity currently trades with a redemption yield – the annual return if held till maturity – of 5.8%. The last time it did so was back in May 1998. The more commonly quoted 10-year gilt yield, currently 5.14%, was last this high in 2007, just before the Global Financial Crisis (GFC).

Since the GFC led to the first use of quantitative easing by the Bank of England to buy government bonds, you could say that we’ve completed a nineteen-year round-trip. That journey took us to a yield low point of 0.07% in August 2020, again thanks to central bank purchases and the fact that the bank base rate was 0.1%. To put that into context, a yield of 0.07% meant that it would take 1,420 years to earn back your capital through interest payments!

And the country’s finances relative to 2022? In some ways, not markedly different. The debt-to-GDP ratio is similar, at around 94%. However, higher interest payments on the outstanding debt will create an increasing burden as gilts issued in the last nineteen years mature and have to be refinanced at higher rates. At least the government is aware this and has been at pains to rebuild some fiscal headroom by increasing taxes. But, of course, that has weighed on economic growth.

A trend shift

Unlike today, bond yields were trending downwards in both 1998 and 2007. The 10-year yield had peaked at over 16% in 1980 and then again at close to 13% in 1990 in the face of high inflation. It’s difficult to overemphasize the positive influence of falling bond yields on the equity bull market that ran from 1980 to 2000. Bond yields constitute the discount rate used by investors to value future streams of earnings. The figure they come up with is called ‘net present value’. A lower yield leads, arithmetically, to a higher net present value for those earnings. That two-decade period saw balanced portfolio investors reap substantial gains from both equities and bonds, while inflation trended lower thanks to factors such as productivity growth and increasing globalisation.

However, bond yields can get too low for comfort. Very low yields can also signal insufficient growth or the risk of tipping into Japan-style deflation. If prices are driven lower by innovation and productivity enhancements, this might be deemed ‘good’ deflation. But insufficient demand meeting oversupply is the bad sort. That was the world that threatened to develop after the technology bust at the turn of the century. It was later reinforced by the 2008 GFC, after which households and governments were more inclined to reduce their debts than to increase spending.

The first two decades of the century didn’t turn out too badly for investors, especially on a risk-adjusted basis. Central banks’ quantitative easing supported financial assets, and the volatility of balanced portfolios was dampened by the fact that bonds’ and equities’ performance wasn’t positively correlated. To the contrary, when one went up, the other went down.

That relationship has shifted again since the pandemic. Governments, bowing to populist forces, have been more willing to spend. That tendency has been reinforced by geopolitical events, including the war in Iran. Inflation has kicked into a higher gear.

Although we endured a painful resetting of valuations in 2022, higher inflation hasn’t hindered equity markets – they hit new all-time highs again last week. So far, the tailwind of strong growth in corporate earnings has proved more powerful than the valuation headwind of a higher discount rate. To some degree, this has been enabled by the incredible level of investment in artificial intelligence (AI), which looks sustainable for the foreseeable future. But we have to consider the possibility that the bond market’s influence proves more potent. After all, the AI-related capex is inflationary in its own right. For example, the latest producer price data in the US showed a 27% year-on-year increase in the cost of electronic components. Much of this can be pinned on the burgeoning demand for memory chips as AI-related demand shifts from training the large language models to using them (a process known as inference).

A crowded boat

We could paint this situation more optimistically by saying that the rise in gilt yields isn’t a problem specific to the UK, but you can immediately see the flaw in that line of thought. If bond yields are rising everywhere, that leaves investors with fewer places to hide. And while the UK is paying more than any other G7 country for its debt, the interest bills are rising for the other six too.

This year, the UK 10-year gilt yield’s climb from 4.47% to 5.14% amounts to an increase of 0.67 percentage points (pp). The average yield increase for the other six G7 members is 0.3pp. Since the Iran war began (and yields had been falling before that), the 10-year gilt yield has increased by 0.91pp against an average 0.60pp for the others (with a relatively tight range from 0.51 to 0.68pp).

So investors must see something in the UK they don’t like. Especially since the UK started with a higher yield, thanks to its history of higher structural inflation and the “moron premium” attached to it since the Truss affair.

I think you need look no further than the Labour Party and its leadership contest. With betting markets favouring Andy Burnham as the likeliest winner, investors foresee a shift further to the left in policy that will lead to higher debt issuance. This fear could be exacerbated if, for example, increased defence spending is met outside the fiscal rules, an idea floated by Burnham in April (but it will still need to be paid for).

However, Burnham seemed to allay that fear in Monday comments, suggesting that he has been advised not to ignore the influence of the so-called ‘bond vigilantes’. This is the nickname given to investors in government bonds, who have the capacity to limit governments’ ability to resort to large fiscal deficits. That’s because governments know these bond investors will, in response, sell off bonds in fright, forcing up yields.

The balancing act

We’re almost always weighing opposing forces when constructing portfolios. Today, it feels as though those forces are more extreme than usual. There’s the massive potential reward of the buildout and adoption of AI on one side; there’s the threat of further disruption to energy supplies and inflation on the other.

Boring as it might seem not to bet the farm on one or the other extreme outcome, I’d portray that as responsibility amid uncertainty. Diversified portfolios still offer the best means of navigating the world. We certainly won’t be left behind if the AI boom wins out, but neither will we be left empty-handed if inflation and public finances turn out to be a bigger problem.

UK bond yields have risen particularly fast, on fears that Andy Burnham or another left-wing figure could replace Keir Starmer as premier