Steps to help you stay in control and reduce the risk of running out.

How much money will you need in retirement?

It’s one of the most important and often most difficult questions to answer.

With people living longer and everyday costs rising, even those with significant savings can find their retirement income under pressure. It’s no longer just about reaching a number. What matters is whether your money can support the life you want, for as long as you need it.

Here are seven essential tips to help you plan ahead, protect your wealth and enjoy the freedom you’ve worked hard to achieve.

Quick read: what you need to know

Only have a minute? Here are the seven steps in short:

01

Picture your ideal future.

Think about how you want to spend your time and who you might want to support.

02

Know how much you’ll really need.

Retirement could last 30 years or more. Be

realistic about the income it will take to live the way you want.

03

Check whether you’re on track.

A cashflow plan shows if your savings are likely to last and what you can do if they’re not.

04

Account for rising prices.

Inflation can halve the value of your income over a 30-year retirement. Make sure your investments can keep up.

05

Use all your tax allowances.

Structuring your savings and withdrawals efficiently can help your money go further.

06

Plan early for future care.

Care costs can be high but planning ahead gives you more options and peace of mind.

07

Speak to a planner.

Getting expert advice can help you make smarter decisions and feel more in control.

01

Picture your ideal future

Start with a vision, not just a number.

Retirement no longer follows a fixed path. For some, it means slowing down. For others, it’s a chance to travel, volunteer or take up new interests. Some people continue working in a different way.

Planning for retirement isn’t only about how you want to spend your time. Many people also continue to support their families by helping children with housing deposits, contributing to weddings or caring for grandchildren. These moments are often deeply meaningful but come with financial implications.

The clearer your goals, the easier it is to work out what your retirement might cost. Taking time to think through the lifestyle you want – and who else might depend on you – is the foundation of a strong financial plan.

02

Know how much you’ll really need

Be pragmatic about the cost of retirement.

It’s easy to underestimate the cost of a comfortable retirement. According to the Retirement Living Standards, a single person needs to spend more than £43,900 a year. For a couple it’s £60,600. The amount of savings required to generate enough post-tax income to pay for this depends on how they are managed, when you plan to retire and whether you have other income.

The big unknown is how long retirement will last. A woman aged 60 today can expect to live to 87 on average, with a one-in-four chance of reaching 96 and a one-in-10 chance of living to 99.

For a man the same age, the average life expectancy is 84, with a one-in-four chance of reaching 92 and a one-in-10 chance of living to 96.

Retirement income may need to stretch over 30 years or more. This is before factoring in inflation, healthcare costs or ongoing support for family. Being realistic about the income you’ll need – and how long you might need it – is a crucial step in building a sustainable financial plan for later life.

Estimated annual spending for a comfortable retirement

03

Check whether you’re on track

Use cash flow planning to see where you really stand.

Once you know what kind of retirement you want and what it might cost, the next step is to understand whether your current finances can support it. Cash flow planning can make a real difference.

A financial planner can help you map out your income, assets and spending over time. This exercise creates a personalised picture of how long your money might last and what you can do if there’s a shortfall.

Sometimes, the picture is more positive than expected. You may have more than you need. That could give you the freedom to retire earlier, spend more in the early years or support others while you’re around to enjoy it.

Cash flow planning could make a real difference by using assumptions to project how your finances might support your retirement goals. It brings clarity, and with that, more control over your future.

04

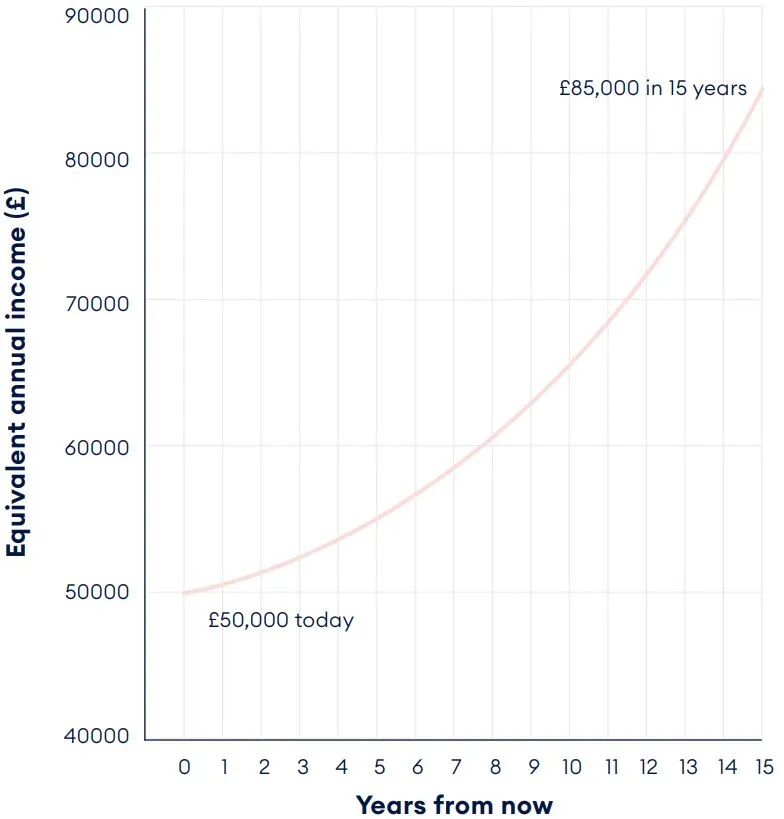

Account for rising prices

Inflation doesn’t stop when you retire.

Rising prices are a concern for everyone, but in retirement they can be especially damaging. Your income may be more fixed, and your savings more exposed to long-term erosion.

According to the UK’s Office for National Statistics (2024), prices have increased by an average of 3.60% a year based on the Retail Prices Index. At that rate you’d need £85,000 in 15 years to maintain the same standard of living.

Inflation affects people differently depending on how they spend their money. If you spend more on food, energy or healthcare, which often rise faster than the average, the impact can be greater.

A financial planner can help you invest in ways that aim to outpace inflation and reduce the risk of your income falling short later in life.

However, you should remember that your capital is at risk when investing and you could lose some or all of your investment.

How inflation erodes income over time

Source: ONS, Retail Prices Index, July 2025

05

Use all your tax allowances

Make tax efficiency part of your plan.

A tax-efficient retirement plan helps your money go further and last longer. Pensions are still one of the most effective ways to save, offering tax relief on contributions and tax-free growth. With the annual allowance (the maximum you can contribute to your pension each year while still receiving tax relief) now increased to £60,000 and the Lifetime Allowance (previously a cap on the total amount of pension savings you could build up without incurring a tax charge) abolished, there’s more flexibility than ever.

Beyond pensions, you can make the most of other allowances:

![]()

Use ISAs for up to £20,000 per year of tax-free savings and investments

![]()

Share income or assets between spouses or civil partners

![]()

Structure withdrawals to minimise income tax and capital gains tax

Depending on your circumstances, your adviser may also explore options such as Venture Capital Trusts (VCTs) and the Enterprise Investment Scheme (EIS), which offer tax incentives in return for higher investment risk. These investments are high risk and not suitable for everyone so it’s essential to seek professional advice before considering them.

The right strategy can give you more freedom in retirement and may help you pass on more to future generations.

The right strategy can give you more freedom in retirement.

06

Plan early for future care

Consider care before you need it.

It’s easy to focus on building your income for retirement and overlook one of the biggest future costs: long-term care.

As life expectancy increases, more people will need some form of care, from help at home to full-time residential support.

The costs can be substantial. On average, residential care in the UK costs more than £64,000 a year, rising to £88,000 for nursing care with dementia in London and the Southeast.

Care planning is about more than money. It’s about peace of mind for you and those close to you.

The Department of Health and Social Care estimates that one in seven people will spend over £100,000 on care during their lifetime.

Planning early can give you more choice about the care you receive and reduce the risk of needing to sell assets under pressure.

A financial planner can help you explore the full range of options, from using savings or investments to downsizing or arranging a care annuity.

07

Speak to a planner

Don’t wait to get expert advice.

Whether retirement feels far off or just around the corner, talking to a financial planner now can help you make better decisions with greater confidence.

You don’t need to know all the answers. An adviser can help you define your goals, assess your current position and build a personalised plan that adapts as your life changes.

Your plan might include planning your income, managing tax, protecting against inflation or thinking ahead to future care needs.

Starting early gives you more flexibility, but it’s never too late to take control of your financial future.

Explore the full retirement planning series

This guide is one of six in our series designed to help you make informed, confident choices about life after work.

Keep more of your money in retirement

How to draw an income tax-efficiently and help your savings go further.

Keep your retirement on track by avoiding these common mistakes

What we see most often and how to avoid it.

Will your retirement savings last if you live to 100?

Why it pays to plan for longer and how to make your money go the distance.