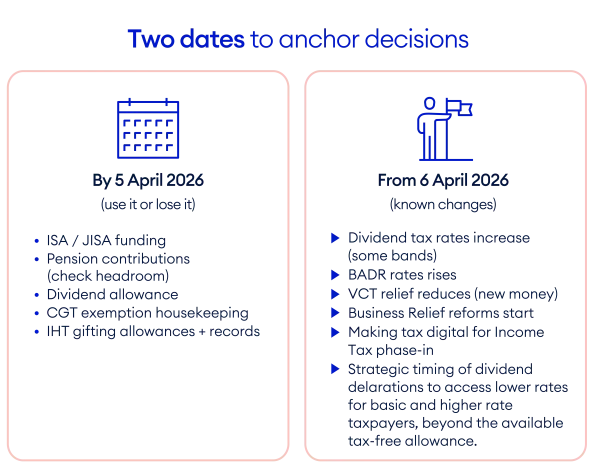

2) Pension funding (personal and employer)

- Annual Allowance is up to £60,000: (taper may apply for high earners).

- Money Purchase Annual Allowance (MPAA): £10,000 if triggered, for example by flexibly accessing defined contribution pension benefits.

- Carry forward: unused annual allowance from the previous three tax years may be available, but requires a headroom check.

Why it matters: For many owners, pension contributions remain one of the largest legitimate levers for improving after-tax outcomes. For owner-managed businesses, employer contributions can be especially attractive. However, structure, timing and documentation matter, so your accountant should be aligned on the corporation tax treatment and payment date.

How we can help

If you are unsure how much headroom remains or how employer contributions interact with your wider plans, we can work with your accountant to confirm what is supportable.

Business-owners lens:

- Where most wealth is illiquid and represented in the unrealised value of the business, pensions can help build “protected capital” outside the trading balance sheet.

- If an exit is approaching, there may be concern that pension contributions reduce reported profits. In practice, those concerns are often overstated

3) Dividends (owner-managed companies): allowance, rates and timing

- Dividend allowance: £500

- Dividend tax rates: for basic and higher rate taxpayers, rates increase by 2 percentage points from 6 April 2026. The additional rate is unchanged.

Why it matters: Where dividend timing is genuinely controllable and properly documented, declaring a dividend before 6 April 2026, if it was going to be taken anyway, may create a modest saving compared with taking the same dividend after 6 April for basic or higher rate taxpayers.

Two practical cautions (where things go wrong):

- Company law / reserves: dividends must be paid out of distributable profits. “Cash in the bank” is not an option.

- Timing and documentation: The relevant tax date is not always the bank payment date. Board minutes, dividend vouchers and clear “payable date” wording are critical, particularly around 5 April.

Couples: Where spouses or civil partners are shareholders, it is worth checking whether each person is using their own dividend allowance and lower rate bands. In some cases, transferring or issuing shares to a lower-rate taxpayer may be considered. This must be consistent with ownership, control and genuine family intent, and professional advice is essential. Capital gains tax implications may also arise.

How we can help

If you would like clarity on whether a dividend before 5 April is commercially coherent and properly evidenced, we can review reserves, documentation and personal tax bands with your adviser team.

4) Capital Gains Tax housekeeping (often smaller, still worth checking)

- Annual exempt amount (AEA): £3,000 (limited - but still use it or lose it).

Why it matters: The exemption is modest, but incremental “maintenance” actions can reduce the eventual chargeable gain, particularly where you also have:

• capital losses that could be used strategically,

• assets you were planning to dispose of anyway, or

• genuine spouse or civil partner planning that fits the wider family position.

Practical caution: avoid simplistic “sell and buy back next day” thinking. Anti avoidance rules can apply and may render such actions ineffective.

How we can help

If you hold investment assets alongside your business interests, we can help coordinate gains, losses and spouse planning to avoid unintended outcomes.

5) Inheritance tax gifting “hygiene ” (simple but commonly missed)

- Annual exemption: £3,000, with one year carry forward only.

- Small gifts: £250 per recipient, subject to conditions.

- Normal expenditure out of income: potentially powerful, but only where it is genuinely regular and affordable. Documentation is critical as it can be complex.

Why it matters: Nil-rate bands are frozen until 6 April 2031, and business asset values often grow faster than allowances. Business Relief remains important, but from 6 April 2026 inheritance tax may arise on business interests above the new £2.5 million allowance for 100% relief. Consistent use of gifting exemptions is rarely dramatic, but it often makes later planning more manageable.

Owner reality check: Gifting is not only a tax decision; it is a control and governance decision. Tax-driven action is most compelling when assets will not qualify for full relief post 5 April 2026, or when transfers of business property exceeding the available allowances are being considered for trust structuring before that date.

How we can help

If gifting is part of your long-term plan, we can help ensure it is structured, documented and aligned with your wider estate strategy.

What changes from 6 April 2026 and why this year-end matters

These confirmed April 2026 changes are most likely to influence "do we act before 5 April?" conversations.

1) Dividend tax increases (basic and higher rate taxpayers)

From 6 April 2026, dividend tax increases by 2 percentage points for the ordinary rate (10.75% from 8.75%) and the upper rate (35.75% from 33.75%). The additional rate remains unchanged.

What it means: For owners in the basic or higher rate bands who have genuine flexibility over dividend timing, and where company law, documentation and distributable reserves support it, bringing forward dividends may be appropriate. Any decision must be commercially coherent and consistent with your overall tax position.

How we can help: We can model the difference and confirm whether action is proportionate to the potential saving.

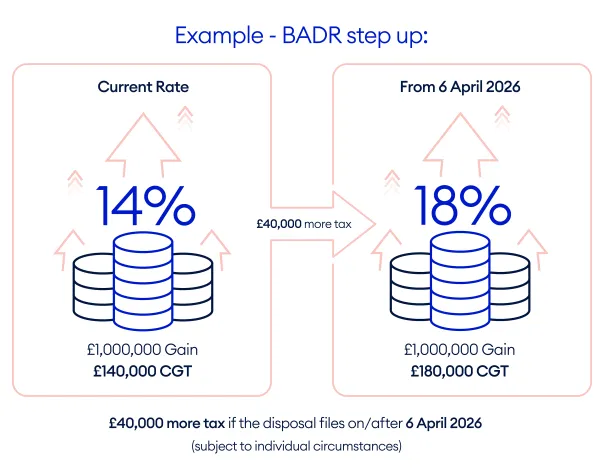

2) Business Asset Disposal Relief (BADR): rate rises again

For qualifying disposals:

• the BADR rate is 14% for disposals made on/after 6 April 2025, and

• it increases to 18% for disposals made on/after 6 April 2026.

The lifetime limit remains £1 million of qualifying gains.

What it means: If a sale or exit is plausible, BADR discussions should not be left to the final weeks. Deal timetables slip frequently, and “we will complete just before 5 April” is rarely realistic.

How we can help: If an exit is even a medium-term possibility, we can work alongside your corporate advisers to sense-check timing risk and tax exposure early.

3) VCT relief reduces from 30% to 20% (new subscriptions)

From 6 April 2026, Venture Capital Trust income tax relief for new subscriptions reduces from 30% to 20%.

What it means: For investors already considering VCTs, and only where suitable, 2025/26 is the final year with 30% upfront relief. VCTs are high risk and illiquid by design. Relief depends on meeting conditions, including holding shares for at least five years.

How we can help: If VCTs form part of your tax planning, we can assess suitability and ensure risk, liquidity and relief conditions are fully understood.

4) Business Relief reforms start on 6 April 2026

From 6 April 2026, reforms to Agricultural Property Relief and Business Property Relief take effect. Key points include:

- A new £2.5 million allowance (per individual) for 100% relief across qualifying APR and BPR combined, with 50% relief above that level.

- 50% relief, rather than 100%, for certain unlisted shares admitted to trading on recognised stock exchanges, often relevant to AIM-type holdings.

What it means: Where Business Relief is central to your estate planning, particularly above the new allowance, ownership structure, documentation and liquidity planning should be aligned well before March. This is rarely a last-minute tax issue; it is a valuation, governance and funding issue.

For a detailed explanation, see our planning for the new £2.5 million Business Relief limit article.

How we can help: If Business Relief exposure is material in your estate, we can help quantify potential inheritance tax exposure under the new regime and coordinate next steps with your legal and tax advisers.

Illustrative example

Example 1 - dividend rate rise:

If a £50,000 dividend is fully taxed at the higher dividend rate, a 2 percentage point increase costs an extra £1,000 of tax (£50,000 × 2%) if taken after 6 April 2026 rather than before, all else equal.

Example - BADR step up:

A £1,000,000 qualifying gain taxed at 14% is £140,000 of CGT.

The same gain taxed at 18% results in £180,000 of CGT.

That is £40,000 more tax if the disposal occurs on or after 6 April 2026. Individual circumstances and deal mechanics will affect the outcome.

Who should pay attention

• Director shareholders who can control dividend timing.

• Anyone considering a business sale in light of the BADR rate change.

• Families with material Business Relief exposure above the new £2.5 million allowance from April 2026.

Do this now: a 30 minute checklist

- Confirm likely 2025/26 income band (basic, higher or additional) and where dividends and gains sit.

- Use ISA allowance and your spouse or partner’s ISA where relevant.

- Check pension headroom, including annual allowance, taper, MPAA and carry forward where relevant.

- For owner managed businesses: review salary and dividend mix and timing. Confirm documentation and cashflow first.

- Consider spouse and partner planning where appropriate and consistent with genuine ownership.

- Review CGT position, including annual exemption and losses. Avoid simplistic “bed and breakfast” outcomes.

- Use inheritance tax annual gifting exemptions and document gifts carefully, including any one-year carry forward of the annual exemption.

- If considering VCTs, and only where suitable, note the reduction in upfront relief from 6 April 2026.

- If Business Relief planning is relevant, ensure actions align with the April 2026 rules and seek advice early.

- If Making Tax Digital Income Tax might apply, select appropriate software and processes in good time.

How we can help: If you would value a short review to prioritise which of these points are genuinely relevant, we can provide a focused pre-year-end discussion.

Now to March 2026

Work out what's relevant and what needs lead time

Some decisions take longer than people expect.

Dividend declarations need distributable reserves confirmed and board process in place. Pension contributions need headroom checks and provider processing time. Use this window to triage which actions genuinely apply to your situation and identify anything with a paperwork tail.

By 5 April 2026

Put agreed actions in place and document them properly.

Make pension contributions, subscribe to ISAs, declare any dividends and complete any planned gifts before 5 April.

Documentation matters as much as timing: board minutes, dividend vouchers and gift records all need to exist before the deadline, not be reconstructed after it.

From 6 April

New tax year - reset allowances, new rules in effect.

Fresh allowances open from 6 April and the new rates and rules are now live: higher dividend tax for basic and higher rate taxpayers, Business Asset Disposal relief at 18% and the revised Business Relief regime.

A short review at the start of the year, rather than the end, is usually the more comfortable way to start ahead of it.